|

Back to Blog

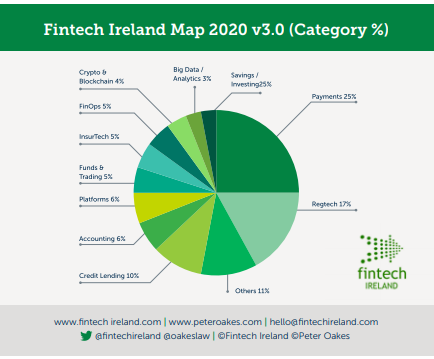

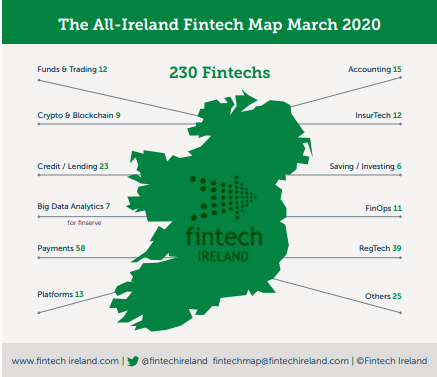

"As I write, the impact on people and businesses arising from the coronavirus is being felt across all parts of society and the economy. It is keeping many of us exceptionally busy not only assisting our clients but dealing with the impacts on our businesses too." Fintech Ireland's and CompliReg's Peter Oakes writes on the The Irish Fintech Ecosystem: Headwinds and Tailwinds (and the Making of a Global Fintech Centre) for CPA Ireland's Accountancy Plus Download the article in PDF and visit CPA Ireland's excellent resources. Continue reading below. Why would one start an article about fintech referencing Covid-19? The fact is that the virus is acting as both a headwind and tailwind for fintech companies operating from Ireland and internationally. The impact of the virus over the last month and a half on fintech has shone a spotlight on many aspects of the ecosystem that might not have otherwise come to our attention. In the current climate Ireland must also be mindful of any potential slippage of its position as a global fintech player garnered from recent years of excellent work. Let’s start with an overview of fintech. The word fintech came to prominence after the last financial crisis, particularly noticeable from 2012 onwards. Yet there were many examples of ‘financial technology’, shortened to “fintech”, existing well before the start of the last financial crisis. A number of these fintech businesses date back to the latter part of the 1980’s. Examples include the internet and phone retail bank First Direct[1] (a division of HSBC) which kicked off in 1989 and today regularly achieves high satisfaction rates in financial surveys. Ireland too served as HQ to a pioneer challenger bank, First-e[2] [6], which despite great promise was a casualty of the dot.com boom[3]. What does the Irish fintech scene look like? The consensus is that Ireland is home to somewhere between 220-250 indigenous fintech companies and that together with international fintech companies in Ireland, the number is probably around 400. It is difficult to give an exact figure if only because the word “fintech” is a broad-church. The word captures, (a) the new nonbank disruptors which focus on discrete parts of the banking value chain, e.g. payments, wealth management, treasury services and credit and lending; (b) the new breed of digital only (non-branch) challenger banks entering both retail and business banking; and (c) the incumbent banks (sometimes referred to as legacy banks) embarking - with various degrees of success – on digital transformation journeys. The recent release in April of the 2020 edition of the Fintech Ireland Map[4] identified 230 indigenous / Irish controlled fintech companies. This was an increase of 30% from the previous year. The Map is supported by both research and a survey[5]. The criteria to meet to join the Map is challenging. Entrants must be fintech companies with a proprietary product or service. Footnotes from above section - 1 https://en.wikipedia.org/wiki/First_Direct 2 https://en.wikipedia.org/wiki/First-e_Group 3 https://www.theguardian.com/money/2001/sep/08/saving.onlinebanking 4 https://fintechireland.com/fintech-ireland-map.html 5 https://fintechireland.com/fintech-survey.html  Broadly speaking the fintech companies operate across 12 categories, being Credit & Lending; Platforms; Funds & Trading; Crypto & Blockchain; FinOps (Financial Operations); InsurTech (Insurance Technology); Accounting; Payments; RegTech (Regulatory Technology); Savings / Investing; Big Data / Analytics; and Others. The number of firms in each category is shown in the diagram below. During 2019, the fintech ecosystem in Ireland, both the Republic of Ireland and Northern Ireland, continued to grow and evolve. There was strong growth in RegTech which not only increased to 39 companies but is rapidly closing in on Payments which retains its crown as the largest category for fintech companies, increasing to 58. It is no surprise that the Irish payments sector is so large given that it powers e-commerce transactions which by 2024 will double from 2010 to €3.8 billion in value. Also boding well for Ireland are two recent reports from UBS which estimate that global e-commerce will grow by 15-20% per annum over the next decade[7] from USD 3 trillion today. It is no wonder that global fintech revenue is expected to reach a staggering USD 500 billion by 2030[8]. The number of fintech firms in the Irish credit and lending sector grew in 2019, with the addition of six new entrants, to 23. This is positive news for cash strapped small-medium size enterprises. Hopefully these fintech companies will help fill the supply of liquidity which is currently in demand by cash-strapped businesses. Headwinds and Tailwinds The coronavirus crisis and its impact upon fintech is no different than the impact of the virus on other sectors of the economy. However, being a broadchurch, there are just as many fintech’s flourishing as there are floundering. FinTech’s, on average, didn’t begin 2020 with large amounts of equity. In fact, before Covid-19 the level of global investment in fintech dropped between 2018-2019 while the level of venture capital investment in Irish fintech fell off a cliff edge. In some cases, Irish fintech companies who had struck deals with international purchasers had to reduce the price to reflect, in the words of one fintech purchaser, the “economic reality” that businesses and individuals are currently facing. E-commerce companies and the fintech companies which process their payments have seen a significant fall in transaction volume and therefore revenue (processing fees) for travel related items, including airfares, hotels, holiday clothing, luggage and pre-paid travel vouchers. Whereas the fastest growing category of products and services includes – no surprises – disposable gloves, bread machines, cough & cold medicines as well as fitness equipment[9]. Thus, be wary about reading too much into e-commerce and payments processing growth, because it is not all good news. Having said that one of the most well-known e-commerce marketplaces specialising in crafted and homespun goods enjoyed a 100+% increase in share price in less than two months owing to demand for face masks! The World Bank predicts that global remittances from wealthy to poorer countries will drop by at least 20% to $445 billion. This represents a loss of a crucial financing lifeline for many vulnerable households. Much of this money is often eaten by fees by various middlemen. It is estimated that between 7% -12% of the money being transferred [10] is swallowed up by bank collection, transfer and receiving fees. Yet remittances are a vital source of income for people in developing countries. The loss of USD 10 from the value chain may mean the difference of food on the table for a family for a week in the poorest of countries. This challenge also provides an opportunity for fintech companies which can perform foreign exchange and international money transfers at a much lower cost than banks. Footnotes from above section - 6 https://en.wikipedia.org/wiki/First_Direct 7 https://www.ubs.com/global/en/wealth-management/chief-investment-office/investment-opportunities/longer-term-investments.html 8 https://fintechnews.ch/fintech/fintech-revenues-to-reach-us500b-by-2030-ubs-research/35500/ 9 https://www.visualcapitalist.com 10 This is a conservative estimate of fees. In some cases, the fees can be higher when cash is being handled at the collection and reception points  Another disruptor in this area is cryptocurrency. Cryptocurrency service providers remit crypto currency11, instead of fiat currency[12], and do so on distributed ledger technology – the most commonly known example being blockchain – which is simply a different set of payment rails than that used by the banks for money movement, such as SWIFT, the UK’s Faster Payments and Europe’s SEPA. Proponents of cryptocurrency for money transfers argue that it is 250 times cheaper on average to use cryptocurrency than traditional banks and is also cheaper than using many fintech apps.

There are less than ten indigenous crypto/blockchain fintech companies operating in Ireland. In recent years they have been joined by about half a dozen large international crypto/ blockchain firms focussed on financial services. Collectively these international companies are valued in the tens of billions of dollars. Like the indigenous companies, these international fintech’s have chosen Ireland to access our highly skilled software engineers, software developers, coders, programmers and data scientists. Noting the Irish government’s support of both blockchain and international financial services, we should expect to see a lot more from this nascent and promising industry in Ireland. Ireland is already perceived as a top global fintech ecosystem. Our challenge is not about reaching the number one spot globally, which simply will not be the case for a small open economy regardless of how progressive we are. Our challenge is to incrementally raise our profile and position year on year and more importantly remain in the upper echelons vis-à-vis our European Union peers. Ireland is home to 10,000+ regulated financial services companies, it is the 4th largest exporter of financial services in the European Union, 250 of the world’s largest financial services institutions have a base here including half of the world’s top 50 banks. With more than 45,000 people employed directly in international financial services, 15% of which work in fintech, is it any wonder that Dublin ranks 5th highest amongst the top 50 European cities according to Findexable Global Fintech Index 2020 and 7th highest ranked EU member state on the OECD’s Ease of Doing Business Index 2019. The future looks bright for Irish fintech. Many of these companies work in regulated markets and a number of these companies are authorised by the Central Bank of Ireland. What they have in common is the need for capital, people and a stable political environment. Ireland benefits from being a member of the European Union. It is an English first speaking language country, enjoys a common law legal system and adheres to the International Financial Reporting Standards. Ireland’s accountancy profession has a lot to offer and gain from Ireland’s fintech ecosystem. Whether it is a young fintech start-up requiring business and financial advice, seed funding, interim CFO services or larger fintech operator with important financial, taxation and HR strategic planning needs, a competent accounting professional is not only the corner stone but indeed the foundation of a successful and sustainable fintech. Footnotes from above section - 11 Examples of two cryptocurrencies include bitcoin and ethereum 12 Fiat currency is legal tender backed by a government, such as USD, EURO and GBP

0 Comments

Leave a Reply. |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]