|

Back to Blog

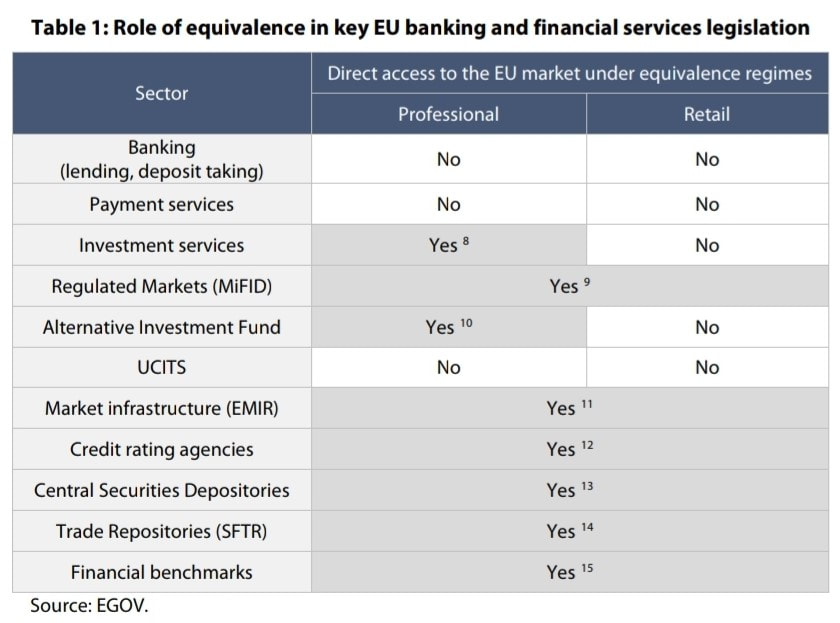

Some choice headlines in the papers about Brexit in the past week as we - according to Brexit Ireland's countdown to Brexit clock - just little more than 33 days before 11p.m. (UK time) on Thursday 31st December 2020 when the Brexit transition period ends with no deal on financial services in sight. This week sees the EU negotiating team returning to London after face-to-face talks came to end more than a week ago after Mr Bariner's team was hit by a case of Covid. They will be greeted by headiness such as: UK dismisses ‘derisory’ EU fishing offer ahead of last-ditch trade talks; Europe’s finance sector hits ‘peak uncertainty’ over Brexit; and The City braces for Brexit.  There is no equivalence regime provided for within either EMD2 (electronic money institutions) or PSD2 (payments services institutions)! One thing we are still very surprised by is the many in #fintech, #techfin and indeed #finserv (and scarily their advisers) who think that recent news on 'equivalence' deals are applicable to all UK #finserv which passport across the European Union / EEA. The announcement on Monday 23rd November by the European Commission was simply and specifically about European regulators finalising a late change seeking to avoid chaos in £15tn of derivatives contracts held between UK and EU counterparties. Then on Wednesday 25th, they insisted outposts of EU banks in London would have to trade certain derivatives in the EU. Back in August 2020 the European Parliament reminded that "Equivalence decisions are a unilateral decision by the Commission. The Commission ultimately exercises its discretion as conferred upon it by the “empowerment” given in EU sectoral legislation.'' BUT MORE IMPORTANTLY "The Commission also enjoys discretion to withdraw equivalence decision. The equivalence frameworks in force do not provide as such specific procedures for monitoring, reviewing or amending equivalence decisions." There are no equivalence provisions in EU bank, payments nor electronic money directives, and the equivalence provision in MiFiD doesn't apply to retail investment services. See the below table on the 'Role of equivalence in key EU banking and financial services legislation' for confirmation. The upshot is that if you are a UK authorised payments institution or electronic money intuition, come Thursday 31st December 2020 when your ability to passport across the whole of European Economic Area comes to an end, so too does your business model unless you have obtained an authorisation in an EU/EEA state. There are are other options available but we'll leave that for another article. If you are a regulated fintech looking for a home post #brexit contact https://complireg.com/authorisations.html. Read our Fintech Authorisation Guides published jointly by CompliReg and Fintech Ireland on the authorisation process. And check out the 'Why Ireland for Fintech' brochure. Why Ireland for your regulated fintech?

“From January 1st, EU rules will apply to UK firms wishing to operate in the EU. UK firms will lose their financial passport: it’ll be anything but business as usual for them. This means they will have to adhere to individual home-state rules in each and every member state,” the official said.  Further reading:

26 November 2020 - Move to EU or face disruption, City of London is warned

27 August 2019 - "Third country equivalence in EU banking and financial regulation"

29 July 2019 - Financial services: Commission sets out its equivalence policy with non-EU countries 12 July 2017 - "Third-country equivalence in EU banking legislation"

|

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]