|

Back to Blog

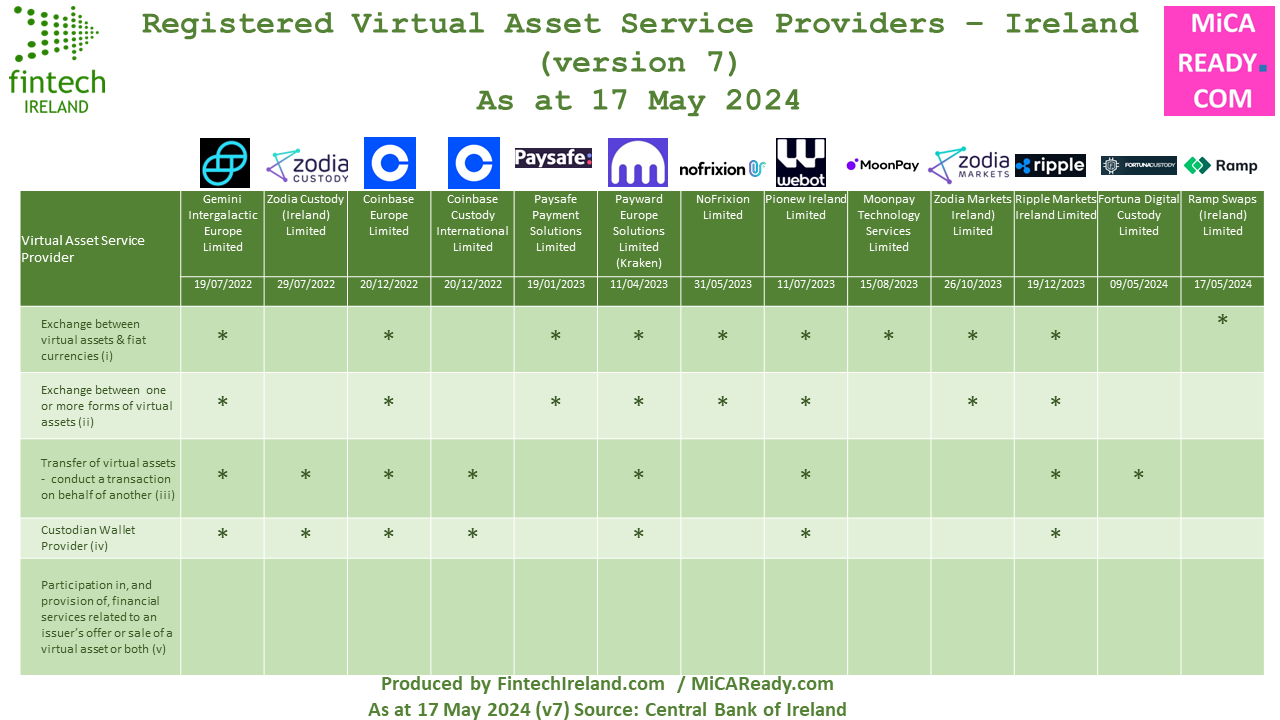

Central Bank of Ireland lays out its expectations of firms seeking crypto licensing in Ireland29/5/2024  If you are looking to get authorised under Markets in Crypto Asset Regulation (MiCAR) in Ireland, the Central Bank of Ireland has confirmed (or perhaps reconfirmed in some people's minds) that regulator intends to open its MiCAR authorisation gateway in early QUARTER 3 2024. While VASPs operating under the VASP regime prior to 30 December 2024, under MiCAR, will be permitted, post 30 December 2024, to avail of a transitional period enabling them to continue to operate for up to 12 months or until their CASP authorisation is granted or refused, whichever is sooner the CBI says that in respect of firms not yet registered as VASPs its experience is that period of at least ten months is required to conclude the assessment of a VASP application. The CBI says such firms should focus their efforts on preparing for a CASP application (under MiCAR) rather than seeking a VASP registration at this time. For those VASPs that have already applied for a registration but have not reached the end point of the process, the CBI will continue to assess these applications and will engage bilaterally with these firms on the progress of their applications. Following Ramp Swaps (Ireland) Limited's registration as a VASP, the latest such registration in Ireland, there are now 13 registered virtual asset service providers in Ireland and potentially a few more to come. Get in touch with CompliReg and see MiCA Ready if you are looking to get a MiCAR authorisation in Ireland or elsewhere in Europe.  Firms looking to get authorised in Ireland as a CASP or registered in near future as a VASP should note the following extracts from a speech today by Gerry Cross, Director for Financial Regulation, Policy and Risk at Blockchain Ireland's excellent event this week (see link at end of article)

Source: Technological innovation and financial regulation – a maturing relationship - Remarks by Gerry Cross, Director for Financial Regulation, Policy and Risk, Wednesday 29th May 2024 Linkedin Post: https://www.linkedin.com/posts/peteroakes_micar-virtualasset-activity-7201513163152834560-N6m7

0 Comments

Back to Blog

The announcement in the media that Coinbase is selecting Ireland as its EU regulatory headquarters has sparked quite a lot of discussion in crypto regulatory circles. Myself and a few others have been thinking about similarities between the race for a MiCAR authorisation [either from a standing start or from the position of already being a Virtual Asset Services Provider registrant in the EU] and the race for UK regulated firms needing an EU home post Brexit. In particular, I recall certain member states doing road shows on why a UK regulated firm should choose its country. While in Ireland, when challenged by the representative bodies and gatekeepers about doing more, the Central Bank of Ireland responded in speeches that it was in no one's interest to get involved in a race to the bottom. Will we not see something similar when it comes to MiCAR? Just because company A has a VASP registration in EU country A, it could make sense but, it doesn't necessarily follow that it will pursue a MiCAR authorisation in EU country A. That is more so the case, arguably, when they have VASP registrations in EU countries B, C and others (because there is no passporting). Therefore, and I am already seeing it myself, there are EU countries laying out their stall for your MiCAR authorisation regardless if you are (or not) already registered there as VASP. Some EU countries argue that their current VASP registration (& remember it was only ever intended to be a mere registration) is so robust and already aligned to MiCAR that you will find its offering a fast, efficient & effective way to getting the authorisation crown. I suspect other member states might take a political or supervisor risk-based decision not to exceed their obligations when dealing with a MiCAR authorisation and - potentially adding things into the authorisation process - to unintentionally but effectively killing-off an application. And, while it is great to hear of a large digital asset player laying down the marker that Ireland will be its EU regulatory home, I have lost count of how may MiFID, emoney and payment firms that have told me that "Ireland is the only country for our company", only to find that their view changes during the course of the authorisation process for whatever reason. I've seen companies apply elsewhere while pursuing an application in Ireland and I have spoken to some of those companies 18 months latter when they discovered the grass wasn't greener in the other EU member state. Against that backdrop, very interesting to read the Chair (Verna Ross) of European Securities and Markets Authority (ESMA) letter of 17 October 2023 to Nadia Calviño President of the Economic and Financial Affairs (ECOFIN) Council of the European Union, saying a number of important things about the MiCAR authorisation infrastructure. Of the many points made by ESMA in its letter, the following ones caught our eye.

The letter was cced to:

* Mairead McGuinness, Commissioner in charge of Financial Stability, Financial Services and Capital Markets Union, European Commission; * Irene Tinagli, Chair of the Committee on Economic and Monetary Affairs, European Parliament; * John Berrigan, Director-General, DG Financial Stability, Financial Services and Capital Markets Union, European Commission; * Thérèse Blanchet, Secretary-General of the Council of the European Union Union; * Claudia Lindemann, Head of the Secretariat of the Committee on Economic and Monetary Affairs, European Parliament

Back to Blog

Australia to regulate digital asset platforms

Regulating digital asset platforms - Australia What is this about? The Australian government intends to introduce a regulatory framework to address consumer harms in the crypto ecosystem while supporting innovation. The introduction of a regulatory framework for entities providing access to digital assets and holding them for Australians and Australian businesses is an important step in the government’s approach to crypto reform in the Australian context. The proposed regulatory framework would apply to digital asset platforms that present similar risks to entities that operate in the traditional financial system. It proposes to leverage the Australian financial services framework to regulate digital asset platforms to ensure consistent oversight and safeguards for consumers. The government seeks views from interested parties on the proposed framework for regulating digital asset platforms. Specific consultation questions are outlined within the paper. Responding You can submit responses to this consultation up until 01 December 2023. Interested parties are invited to comment on this consultation. While submissions may be lodged electronically or by post, electronic lodgement is preferred. For accessibility reasons, please submit responses sent via email in a Word or RTF format. An additional PDF version may also be submitted. All information (including name and address details) contained in submissions will be made available to the public on the Treasury website unless you indicate that you would like all or part of your submission to remain in confidence. Automatically generated confidentiality statements in emails do not suffice for this purpose. Respondents who would like part of their submission to remain in confidence should provide this information marked as such in a separate attachment. Legal requirements, such as those imposed by the Freedom of Information Act 1982, may affect the confidentiality of your submission. Key Documents

How To Respond

Financial System Division Treasury Langton Cres Parkes ACT 2600 Further Reading: https://treasury.gov.au/consultation/c2023-427004

Back to Blog

Fintech UK is looking to partner with registered / regulated (or soon to be) cryptoasset firms on building out a cryptoasset section on our website. If you are senior executive at a UK registered cryptoasset firm, please contact us here to discuss the proposed project. Also happy to hear from senior executives at businesses which support crypto firms to support the project. See our CRYPTO page for more information If you are are crypto firm seeking regulatory advice or director services, please contact CompliReg for assistance at the details appearing here and check out its VASP registration and other authorisation services here. Hope you like the Map (Version 6.0)! Welcome to the version 6.0 of Fintech UK's and CompliReg's (a leading provider of fintech consulting services to crypto asset firms) UK FCA registered Cryptoasset Firms Map.

There are now 41 registered Cryptoasset firms appearing on the Financial Conduct Authority's (FCA) website as at Saturday 31st December 2022. Joining Version 6.0 are three new entrants - Tullett Preborn (Europe) Ltd, MoonPay (UK) Ltd and Hidden Road Partners CIV UK Ltd. The FCA register records their registrations effective 21st November, 9th December and 20 December 2022, respectively. As we continue to Map registered Cryptoasset firms, expect to see certain logos appear more than once as several brands will be registering several Cryptoasset firms for different purposes, such as - for example - services for (1) trading and (2) custody. An example of this is in fact Zodia. While Zodia Markets (UK) Limited was registered on 27 July 2022, its affiliate Zodia Custody Limited was registered effective 15 July 2021. At the time we released Version 1, there were 218 (thereabouts) unregistered cryptoasset business listed on the UK FCA's website that appear, to the FCA, to be carrying on cryptoasset activity, that are not registered with the FCA for anti-money laundering purposes. As of today (01 April 2023), that number has decreased to 82. The firms thus far registered by the FCA include: 2020: Archax Ltd, Gemini Europe Ltd, Gemini Europe Services Ltd, Ziglu Limited, Digivault Limited, 2021: Fibermode Limited, Zodia Custody Limited, Ramp Swaps Limited, Solidi Ltd, Coinpass Limited, CoinJar UK Limited, Trustology Limited, Commercial Rapid Payment Technologies Limited, Iconomi Ltd, Skrill Limited, Paysafe Financial Services Limited, Crypto Facilities Ltd, Fidelity Digital Assets LTD, Payward Limited, Galaxy Digital UK Limited, BABB Platform Ltd, BCP Technologies Limited, Zumo Financial Services Limited, Baanx.com Ltd, Bottlepay Ltd, Genesis Custody Limited, Altalix Ltd, 2022: X Capital Group Limited, Enigma Securities Ltd, Light Technology Limited, eToro (UK) Ltd, Uphold Europe Limited, Wintermute Trading LTD, Rubicon Digital UK Limited, DRW Global Markets Ltd, Zodia Markets (UK) Limited, Foris DAX UK Ltd (aka Crypto.com), Revolut Ltd*, Tullett Preborn (Europe) Ltd, MoonPay (UK) Ltd and Hidden Road Partners CIV UK Ltd. * Revolut group still has not achieved its much talked about ambition of securing a bank authorisation in the UK. We are looking forward to seeing how many more will be registered during 2023. Thus far, there have been no registrations in 2023. The post accompanying Version 6 appears at:

Further Reading: Version 1 of the Map and the Blog of 20 December 2021 - located here Version 2 of the Map and the Blog of 18 July 2022 - located here Version 3 of the Map and the Blog of 28 July 2022 - located here Version 4 of the Map and the Blog of 20 September 2022 - located here Version 5 of the Map and the Blog of 26 September 2022 - located here List of Unregistered Cryptoasset Businesses as at today - located here

Back to Blog

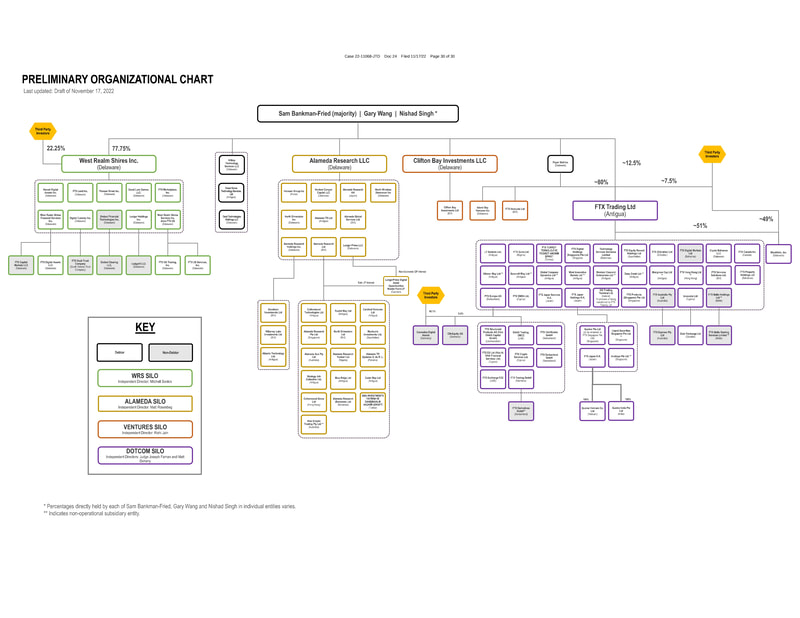

FTX Trading Ltd US Bankruptcy Court for the District of Delaware: Declaration by John J Ray III18/11/2022  Further to my post on Linkedin, here is access to a better quality image of the group structure of FTX. The image above should be of high quality. Otherwise see page 30 in the DECLARATION OF JOHN J. RAY III in support of Chapter 11 Petitions and First Day Pleadings.

The Guardian leads with "New FTX boss, who worked on Enron bankruptcy, condemns ‘unprecedented failure’"

Posted by: Peter Oakes, Founder of CompliReg a leading specialist governance, regulatory and compliance strategy firm. Peter established and led the Enforcement and AML/Supervision Directorate of the Central Bank of Ireland as its inaugural Assistant-Director General, then later Director of Enforcement and AML/CFT Supervision.

Back to Blog

CompliReg, your first choice for regualtory authorisations, licences and registrations is proud to support Fintech UK and its endeavours to Map the FCA registered cryptoasset market in the UK. Fintech UK is looking to partner with registered / regulated (or soon to be) cryptoasset firms on building out a cryptoasset section on our website. If you are senior executive at a UK registered cryptoasset firm, please contact us here to discuss the proposed project. Also happy to hear from senior executives at businesses which support crypto firms to support the project. See our CRYPTO page for more information If you are are crypto firm seeking regulatory advice or director services, please contact CompliReg for assistance at the details appearing here and check out its VASP registration and other authorisation services here. Hope you like the Map (Version 4.0)! Welcome to the second edition (version 4.0) of Fintech UK's and CompliReg's (a leading provider of fintech consulting services to crypto asset firms) UK FCA registered Cryptoasset Firms Map.

There are now 37 registered Cryptoasset firms appearing on the Financial Conduct Authority's (FCA) website as at Tuesday 16th August 2022. Welcome to Crypto.com. The FCA register records Foris DAX UK LTD (aka Crypto.com) registration effective 16th August 2022. At the time Version 1.0 was released there were 218 (thereabouts) unregistered cryptoasset business listed on the UK FCA's website that appear, to the FCA, to be carrying on cryptoasset activity, that are not registered with the FCA for anti-money laundering purposes. As of today (20 September 2022), that number has decreased by one to 247. On both 18th and 28th July 2022 the figure was 248. Read more at Fintech UK on facts and figures about the cryptoasset firms appearing on Version 4.0.

Back to Blog

Click for larger image Fintech UK is looking to partner with registered / regulated (or soon to be) cryptoasset firms on building out a cryptoasset section on our website. If you are senior executive at a UK registered cryptoasset firm, please contact us here to discuss the proposed project. Also happy to hear from senior executives at businesses which support crypto firms to support the project. See our CRYPTO page for more information

If you are are crypto firm seeking regulatory advice or director services, please contact CompliReg for assistance at the details appearing here and check out its VASP registration and other authorisation services here. Hope you like the Map (Version 2.0)! Don't forget to sign up to our Newsletter (we don't spam) by clicking here. We use MailChimp, which means you can unsubscribe whenever you like. Welcome to the second edition (version 2.0) of Fintech UK's and CompliReg's (a leading provider of fintech consulting services to crypto asset firms) UK FCA registered Cryptoasset Firms Map. There are now 35 registered Cryptoasset firms appearing on the Financial Conduct Authority's (FCA) website as at Monday 18th July 2022. The first 5 of these firms were registered in 2020. According to the FCA's records, the first registered Cryptoasset firm was Archax on 18 August 2020. Then in 2021, the FCA registered 22 crypto firms. Thus far in 2022, the FCA has registered 8 crypto firms. The most recent to be registered is DRW (7 June 2021). As we pointed out when we released Version 1.0 of the Map, 2021 saw a flurry of activity and especially in the last quarter of 2021 when 16 firms received their Cryptoasset registration from the FCA - that was a whopping 60% of the total pool of registered firms at that time. At the current rate, the number of firms registered in 2022 may be less than that in 2021, unless the FCA registers a large pile of crypto firms in the second half of 2022. As we continue to Map registered Cryptoasset firms, expect to see certain logos appear more than once as several brands will be registering several Cryptoasset firms for different purposes, such as - for example - services for (1) trading and (2) custody. At the time we released Version 1, there were 218 (thereabouts) unregistered cryptoasset business listed on the UK FCA's website that appear, to the FCA, to be carrying on cryptoasset activity, that are not registered with the FCA for anti-money laundering purposes. As of today, that number has increased to 248. The firms thus far registered by the FCA include: 2020: Archax Ltd, Gemini Europe Ltd, Gemini Europe Services Ltd, Ziglu Limited, Digivault Limited, 2021: Fibermode Limited, Zodia Custody Limited, Ramp Swaps Limited, Solidi Ltd, Coinpass Limited, CoinJar UK Limited, Trustology Limited, Commercial Rapid Payment Technologies Limited, Iconomi Ltd, Skrill Limited, Paysafe Financial Services Limited, Crypto Facilities Ltd, Fidelity Digital Assets LTD, Payward Limited, Galaxy Digital UK Limited, BABB Platform Ltd, BCP Technologies Limited, Zumo Financial Services Limited, Baanx.com Ltd, Bottlepay Ltd, Genesis Custody Limited, Altalix Ltd, 2022: X Capital Group Limited, Enigma Securities Ltd, Light Technology Limited, eToro (UK) Ltd, Uphold Europe Limited, Wintermute Trading LTD, Rubicon Digital UK Limited and DRW Global Markets Ltd When we released Version 1 we noted that there were 37 firms Cryptoasset firms with Temporary Registration. You will see 39 on the previous list, but two of those firms were in fact registered - thus there seemed to be a timing issue of the records at the FCA. Regardless, some of the 37 achieved FCA registration in 2022 and others have dropped of the current list. Revolut Ltd, as of today, is the only firm listed on the Temporary Registration list and it was listed on December 2021 list too. Interestingly, in addition to a cryptoasset registration, the Revolut group hasn't achieved the obtaining of its much talked about bank authorisation in the UK either. We are looking forward to seeing how many more will be registered before the end of the year. This post also appears at:

Back to Blog

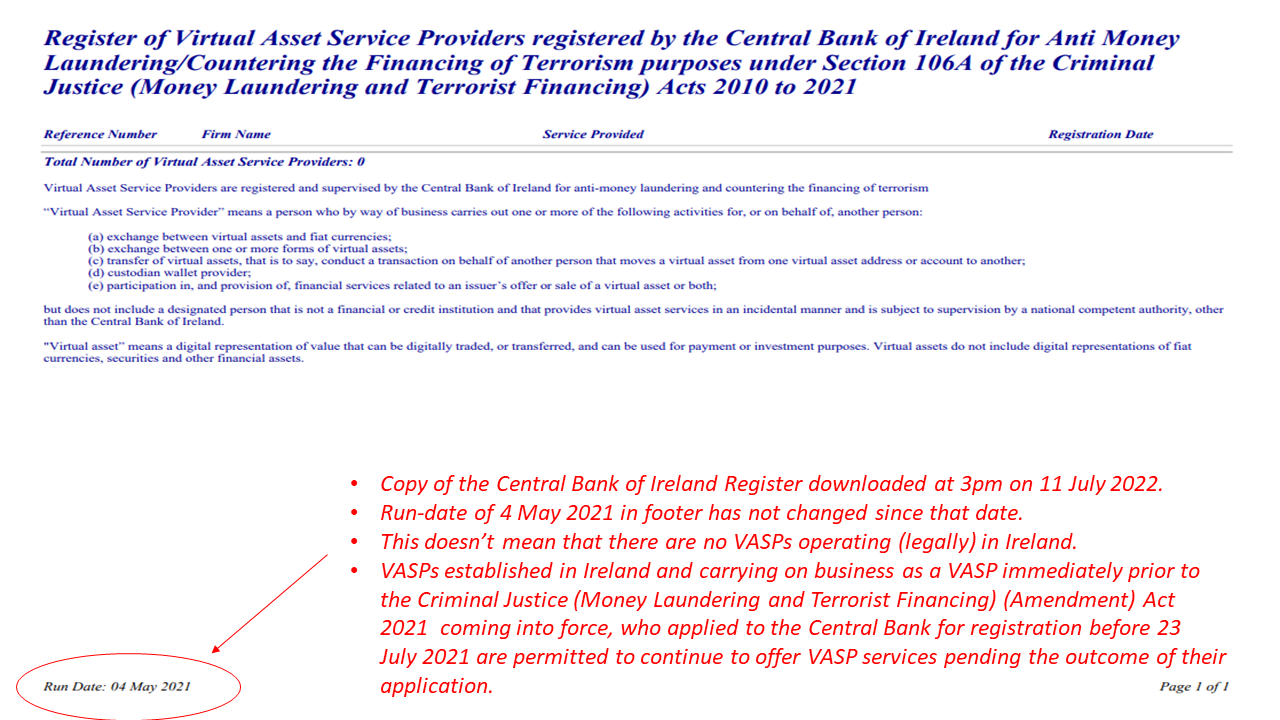

“All current and potential VASP applicants should review the content of the bulletin and take actions to rectify weaknesses, as relevant. Firms undertaking VASP activities are also reminded that a failure to register may result in significant criminal and/or administrative sanctions." Central Bank of Ireland If you need assistance with your Virtual Asset Service Provider registration application, or other regulatory authorisation application such as emoney, payment services or MiFID, get in touch with Peter Oakes at CompliReg by CLICKING HERE. Read more about the Virtual Asset Service Provider registration, emoney authorisation, payment institution authorisation and MiFID authorisation CLICK HERE. Today (Monday 11 July 2022) the Central Bank of Ireland issued a press release highlighting weaknesses in Virtual Asset Service Providers’ (VASP) AML/CFT Frameworks. As of today, according to the Central Bank's website, the total number of VASPs registered in Ireland is ZERO. See image below.  Question: If there are no firms appearing on the register, does that mean that there are no VASPs operating lawfully in Ireland? Answer: No. VASPs established in Ireland and carrying on business as a VASP immediately prior to the Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2021 coming into force, who applied to the Central Bank for registration before 23 July 2021 are permitted to continue to offer VASP services pending the outcome of their application ('transitional period'). While we have heard stories of firms operating as VASPs in Ireland in circumstances where they do not fall under the transitional period, such firms should be subject - if they came to the attention of the Central Bank - to criminal and/or regulatory investigation. Accompanying today's press release is a bulletin in relation to Virtual Asset Service Providers (VASPs), seeking to assist applicant firms to strengthen both their applications for registration and their Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT) Frameworks. The Central Bank says while it seeks to anticipate and support innovation in the financial services industry, firms operating in novel areas must ensure their businesses will not be used to launder the proceeds of crime or to finance terrorism. The Central Bank issued the bulletin to VASPs to assist them in strengthening their applications and frameworks.  Background: Since 23 April 2021, VASPs are required to comply with the relevant AML/CFT obligations under the Criminal Justice Act 2010 to 2021. Any firm wishing to conduct business as a VASP must apply to the Central Bank for registration. The Central Bank says it is currently progressing the assessment of registration applications, and has provided feedback to 90% of applicants on their proposed AML/CFT frameworks. Findings: The Central Bank identified, in the vast majority of applications:

See below for further details on the Central Bank's 'findings' observations. The Central Bank reported that the lack of compliance, coupled with control weaknesses, resulted in a significant number of the applicant firms not being able to demonstrate that they could meet their AML/CFT obligations. Actions: The Central Bank has reconfirmed that it will only register a firm when it is satisfied that the firm can meet its AML/CFT obligations on an ongoing basis. It has said that all current and potential VASP applicants should:

The Central Bank also too the opportunity to remind that:

Key Central Bank observations on registrations received and assessed to dateIncomplete Applications: A number of registration applications did not contain the required information and documentation and consequently such applications did not progress to the assessment phase.

Assessment Phase: In undertaking its assessment of registration applications, the Central Bank noted recurring fundamental issues preventing approving of registration applications as the applicants could not meet their AML/CFT legislative obligations or the Central Bank’s expectations. The Central Bank communicated its concerns and expectations to the applicants for further consideration. The Central Bank helpfully provided a couple of pages in its bulletin (pages 4 - 6) giving an overview of recurring issues identified during the assessment of VASP registration applications. These are repeated below. Money Laundering and Terrorist Financing (ML/TF) Risk Assessment: An effective AML/CFT control framework is built on an appropriate ML/TF risk assessment that focuses on the specific ML/TF risks arising from the firm’s business model. This risk assessment should drive the firm’s AML/CFT control framework such that it ensures there are robust controls in place to mitigate and manage the specific risks identified through the risk assessment. The Central Bank identified a significant number of issues with the ML/TF risk assessments conducted by VASP applicant firms, including:

Policies and Procedures: When developing AML/CFT policies, controls and procedures (“AML/CFT P&Ps”), firms should maintain a detailed documented suite of AML/CFT P&Ps, which are:

The Central Bank identified a number of recurring issues with the AML/CFT P&Ps submitted by applicant firms including;

Customer Due Diligence (“CDD”): CDD involves more than just verifying the identity of a customer. Firms should collect and assess all relevant information in order to ensure that the firm:

The Central Bank identified a number of recurring issues with the CDD AML/CFT P&Ps submitted by applicant firms including;

Financial Sanctions Screening: The Central Bank’s expectation is that firms have an effective screening system in place, appropriate to the nature, size and risk of their business. In addition to this, firms should have clear escalation procedures in place to be followed in the event of a positive match.

Outsourcing: A firm can outsource certain AML/CFT Functions, but are reminded that the firm remains ultimately responsible for compliance with its obligations under CJA 2010 to 2021. It is expected that, where firms outsource AML/CFT functions, a documented agreement is in place that clearly defines the obligations of the outsource service provider. Firms should also evidence that sufficient oversight is conducted on the outsourced activity. A number of VASP applicant firms outsource certain AML/CFT functions to group-related parties and/or non-group related parties.

Individual Questionnaires for proposed Pre-Approval Controlled Function role holders: A number of firms have failed to or delayed in submitting Individual Questionnaires (IQs) for each of their proposed Pre-Approval Controlled Function (PCF) role holders. IQs should be submitted for each individual proposed to hold a PCF role as soon as practical. The Central Bank’s expectation on a firm’s presence in Ireland. In line with the principle of territoriality enshrined in the EU AML Directives and Section 25 of the CJA 2010 to 2021, the Central Bank expects a physical presence located in Ireland and for there to be at least one employee in a senior management role located physically in Ireland, to act as the contact person for engagement with the Central Bank. In addition, in accordance with Section 106 H of the CJA 2010 to 20212 , the Central Bank may refuse an application where the applicant is so structured, or the business of the applicant is so organised, that the applicant is not capable of being regulated to the satisfaction of the Central Bank. Further Reading: Press Release - Central Bank highlights weaknesses in Virtual Asset Service Providers’ AML/CFT Frameworks 11 July 2022

Back to Blog

Key Findings of Cyprus National Risk Assessment with respect to Virtual Assets and Virtual Asset Service Providers (November 2021)Key Findings:

Recommended Actions:

Back to Blog

Click image for larger picture UK Registered Cryptoasset Map Version 1.0 |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]