|

Back to Blog

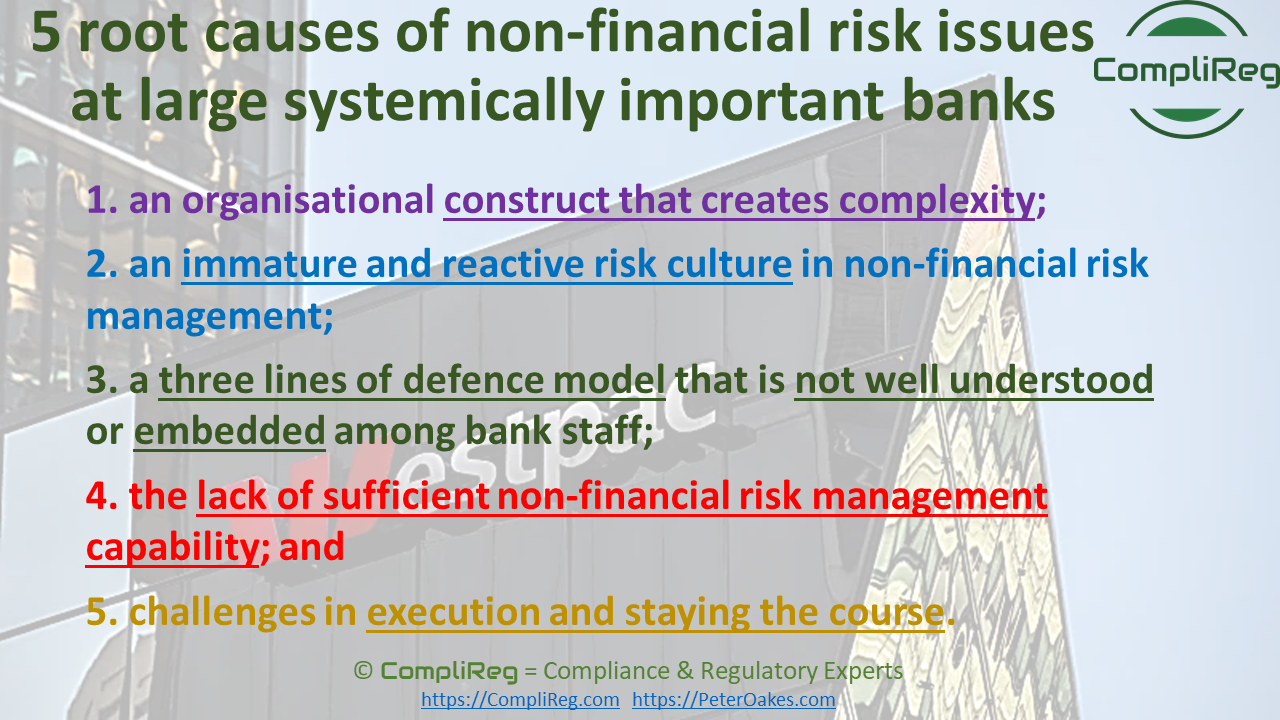

5 point list of root causes of non-financial risk issuesDownload Westpac's Report released 17 July 2020 - Reassessment of the Culture, Governance and Accountability Remediation Plan Linkedin Post at https://www.linkedin.com/posts/peteroakes_riskculture-riskmanagement-regtech-activity-6689803983407628288-ynbv Here's a good 5 point list of root causes of non-financial risk issues at large systemically important banks & institutions (anywhere in the world). In this case Westpac, arising from a report ordered by the Australian prudential regulator. Applicable to non banks and non systemically important institutions:

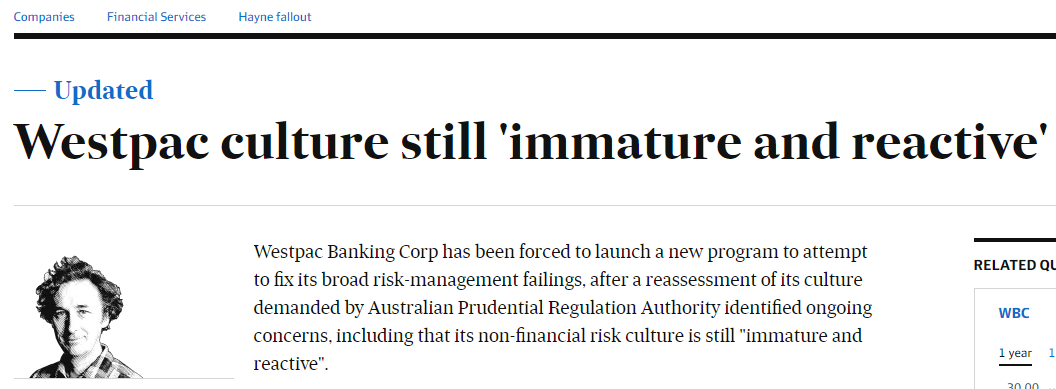

With Westpac's CEO responsible for its new initiative "customer outcomes and risk excellence" or CORE, #regtech will need to feature heavily in execution, tracking & learnings. Professor Elizabeth Sheedy, a #riskculture expert saying that the latest report shows too often risk is seen as a handbrake by banks rather than an enabler for long-term success. Westpac "admitted the "culture, governance and accountability program", set up in January 2019 to implement the reforms, "has not delivered sufficient momentum", with many in the bank still do not "fully appreciate the cumulative impact of the issues". Paul McCarthy Westpac culture still 'immature and reactive' 17 July 2020 Copyright with Australian Financial Review and James Eyers

Westpac Banking Corp has been forced to launch a new program to attempt to fix its broad risk-management failings, after a reassessment of its culture demanded by Australian Prudential Regulation Authority identified ongoing concerns, including that its non-financial risk culture is still "immature and reactive". The new report identifies a lack of urgency and clarity in Westpac's response to problems it identified in a 2018 self-assessment of governance, which were exacerbated when AUSTRAC dropped a bombshell case last November that triggered the departures of the bank's CEO and chairman. The Australian Prudential Regulation Authority insisted on the reassessment because it was concerned Westpac was not tackling the root causes of its failings when it read AUSTRAC's statement of claim. The latest investigation found Westpac is still "overly complex, which results in confusion around accountability and challenges in execution". The shortcomings identified in the report, which was sent to all of Westpac's 35,000 staff on Friday morning, found Westpac's organisational structure created complexity, and its 'three lines defence' model, which is supposed to prevent risks materialising, "is not well understood or embedded". The report highlights a "shortfall in sufficient non-financial risk-management capability" and says that even though Westpac has made various changes to respond to issues, "what is required is a program of deeper change". It criticised an ongoing blame game, stating a priority for its work on culture "will be to strengthen psychological safety" for staff after the reassessment found "in some situations leaders had reacted to incidents with a focus on who is to blame rather than what to learn". Many of the same failings were identified in the bank's self-assessment for APRA in 2018, after all banks were asked to audit themselves against the prudential regulator's expectations for fixing widespread cultural problems at Commonwealth Bank of Australia. The Hayne royal commission should also have emphasised the urgency of repairing culture to meet community expectations and restore trust. But Westpac recognised on Friday the changes it has been making to respond to the 45 recommendations set out in its 2018 self-assessment had been "incremental". It admitted the "culture, governance and accountability program", set up in January 2019 to implement the reforms, "has not delivered sufficient momentum". It said many in the bank still do not "fully appreciate the cumulative impact of the issues". “Our reassessment confirms that our management of non-financial risk is currently not at the standard we set for ourselves," said Westpac CEO, Peter King, releasing the 50-page report to the ASX. “It is clear we have more to do to address these shortcomings, including improving our risk management capability and risk culture which is not where we want it to be." APRA is continuing to investigate possible breaches of the Banking Act by Westpac, including the speed at which it has rectified issues identified by AUSTRAC. APRA has already imposed a $1 billion capital penalty on the bank to reflect its "heightened operational risk profile". At the CORE Westpac on Friday announced it would initiate a multi-year, multi-million dollar program, which it is calling "customer outcomes and risk excellence" (CORE). Mr King said he would be accountable for its delivery. The reassessment said Mr King, who replaced Brian Hartzer as CEO, and the Westpac board, now led by John McFarlane who took the reins from Lindsay Maxsted, need to take more responsibility and set a proper "direction and tone" about the importance of the measures. The report – which was conducted by Westpac management and a team from consultants Oliver Wyman together with assurance oversight by another consulting firm, Promontory – pointed to five ongoing "root causes" of Westpac's travails. These are: an organisational construct that creates complexity; an "immature and reactive" risk culture in non‑financial risk management; a 'three lines of defence model' that is not well understood or embedded among bank staff; the lack of sufficient non-financial risk management capability; and challenges in execution and staying the course. "Westpac does not underestimate both the magnitude of the changes that are required and the effort involved." Professor Elizabeth Sheedy, a risk culture expert from Macquarie University, said the latest report shows too often risk is seen as a handbrake by banks rather than an enabler for long-term success. "For me it all comes back to excessive focus on short-term profits which is driven by short-term cash bonuses," she said. "There is also a massive shortage of qualified and experienced risk and compliance executives across the industry. Institutions tend to want to keep budgets very tight when it comes to resourcing risk and compliance, which sends a message about organisational priorities." It is expected that Westpac will look to make additional cost savings in order to pay for additional investment that will be required to improve risk systems. The report was released after Mr McFarlane warned in an interview with the Financial Review on Friday that excessive financial regulation could make it more difficult for banks to lend and hamstring the economic recovery. Westpac has been negotiating with AUSTRAC over a potential settlement of the anti-money laundering case, with the financial crimes regulator due to file an amended statement of claim next month to incorporate broader allegations that the bank should have suspected another 270 customers were paedophiles. It is also waiting for a decision from the Australian Securities and Investments Commission on whether it will appeal the bank's responsible lending victory in the full Federal Court last month to the High Court. James Eyers writes on banking, fintech and technology. Based in our Sydney newsroom, James is a former Legal Affairs and Capital editor for the Financial Review Connect with James on Twitter. Email James at [email protected] Source: https://www.afr.com/companies/financial-services/westpac-culture-still-immature-and-reactive-20200717-p55cxa

0 Comments

|

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]