|

Back to Blog

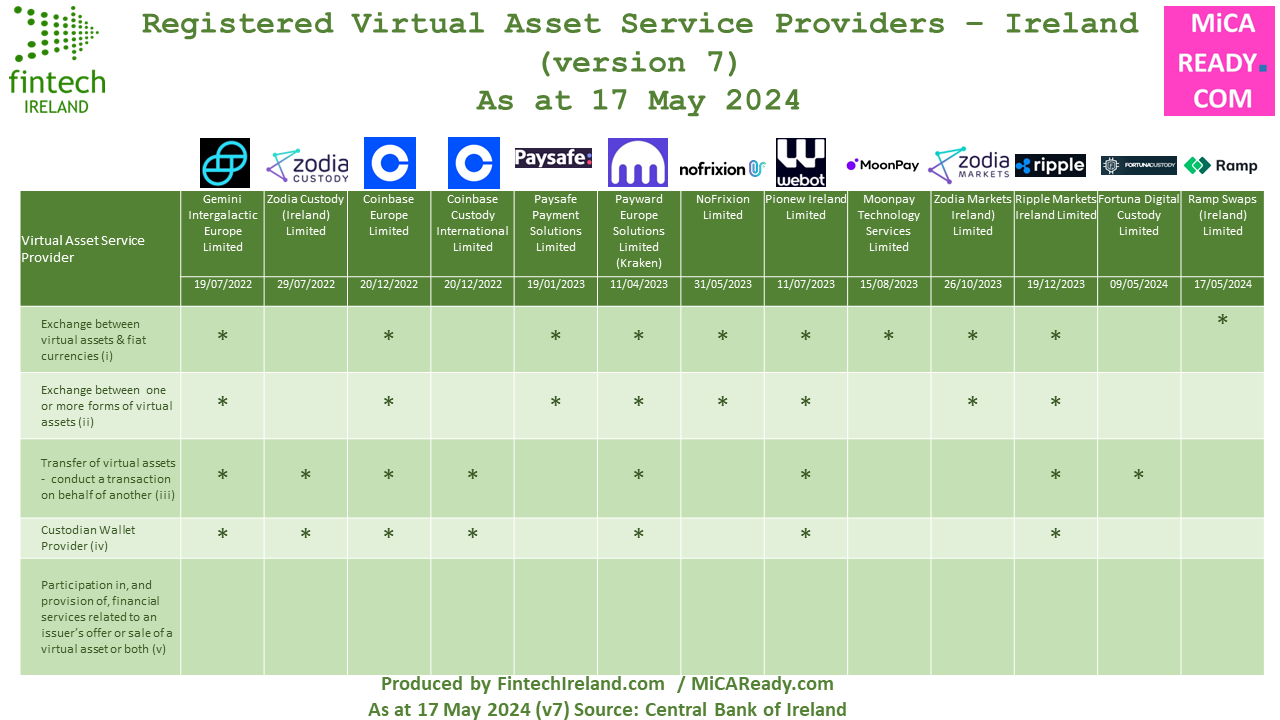

Central Bank of Ireland lays out its expectations of firms seeking crypto licensing in Ireland29/5/2024  If you are looking to get authorised under Markets in Crypto Asset Regulation (MiCAR) in Ireland, the Central Bank of Ireland has confirmed (or perhaps reconfirmed in some people's minds) that regulator intends to open its MiCAR authorisation gateway in early QUARTER 3 2024. While VASPs operating under the VASP regime prior to 30 December 2024, under MiCAR, will be permitted, post 30 December 2024, to avail of a transitional period enabling them to continue to operate for up to 12 months or until their CASP authorisation is granted or refused, whichever is sooner the CBI says that in respect of firms not yet registered as VASPs its experience is that period of at least ten months is required to conclude the assessment of a VASP application. The CBI says such firms should focus their efforts on preparing for a CASP application (under MiCAR) rather than seeking a VASP registration at this time. For those VASPs that have already applied for a registration but have not reached the end point of the process, the CBI will continue to assess these applications and will engage bilaterally with these firms on the progress of their applications. Following Ramp Swaps (Ireland) Limited's registration as a VASP, the latest such registration in Ireland, there are now 13 registered virtual asset service providers in Ireland and potentially a few more to come. Get in touch with CompliReg and see MiCA Ready if you are looking to get a MiCAR authorisation in Ireland or elsewhere in Europe.  Firms looking to get authorised in Ireland as a CASP or registered in near future as a VASP should note the following extracts from a speech today by Gerry Cross, Director for Financial Regulation, Policy and Risk at Blockchain Ireland's excellent event this week (see link at end of article)

Source: Technological innovation and financial regulation – a maturing relationship - Remarks by Gerry Cross, Director for Financial Regulation, Policy and Risk, Wednesday 29th May 2024 Linkedin Post: https://www.linkedin.com/posts/peteroakes_micar-virtualasset-activity-7201513163152834560-N6m7

0 Comments

|

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]