|

Back to Blog

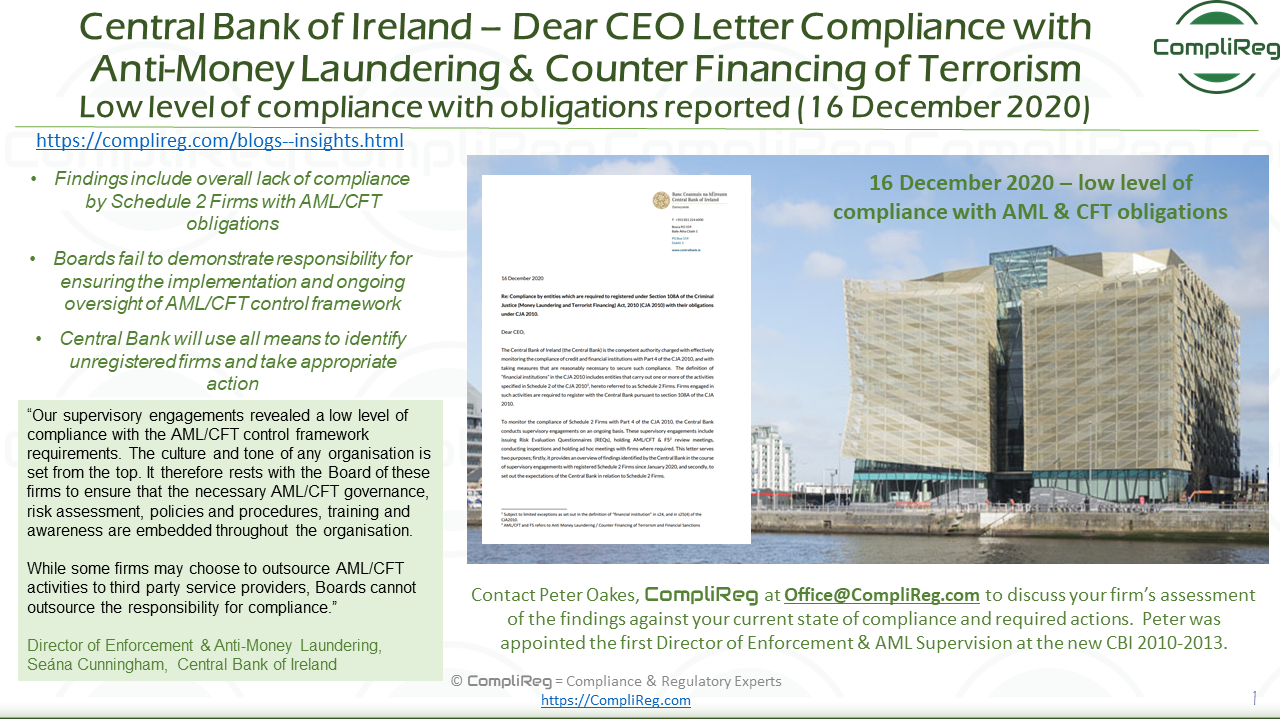

Central Bank publishes “Dear CEO” letter to Schedule 2 firms on low level of compliance with Anti-Money Laundering and Counter Financing of Terrorism obligations

The Central Bank has today (16 December 2020) published the outcome of supervisory engagements undertaken in respect of Schedule 2 Firms to assess compliance with their obligations under Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 (CJA 2010). The "Dear CEO" letter*, outlines the Central Bank’s expectations of firms in relation to Anti-Money Laundering/Counter Financing of Terrorism (AML/CFT) and Financial Sanctions (FS) requirements and details follow-up actions to be taken by CEOs and Boards in response to the findings outlined. The examination, which comprised of both inspections and review meetings, found an overall lack of compliance across all areas of the AML/CFT control framework. There is also poor understanding of the requirements from Board and senior management levels, including at those firms who outsourced their AML/CFT and FS activities to third parties. The examination identified a number of failings across Schedule 2 Firms, including:

Director of Enforcement & Anti-Money Laundering, Seána Cunningham said: “The Central Bank expects all firms to be alert to the risks that money laundering and criminal financial activities may pose to their customers and business, and the wider integrity of the Irish financial system. This requires CEOs and Boards to have in-depth knowledge and understanding of their Anti-Money Laundering and Counter Financing of Terrorism obligations. It is also essential to have the necessary control framework in place to ensure protection of their business and customers. “Our supervisory engagements revealed a low level of compliance with the AML/CFT control framework requirements. The culture and tone of any organisation is set from the top. It therefore rests with the Board of these firms to ensure that the necessary AML/CFT governance, risk assessment, policies and procedures, training and awareness are embedded throughout the organisation. While some firms may choose to outsource AML/CFT activities to third party service providers, Boards cannot outsource the responsibility for compliance. “We will continue to engage directly with those firms where compliance weaknesses and failures have been identified to ensure that they are addressed. We also require all firms to review the content of this letter to ensure that they assess their own compliance with the issues identified. “We are also taking this opportunity to remind all firms to assess their activities to determine if they are required to register with us under Schedule 2. Firms who fail to register are at risk of significant criminal and/or administrative sanctions. In 2021, the Central Bank will use all means available to identify those firms not registered and take appropriate action.” ENDS Notes to Editor

Further information Media Relations: [email protected] / 01 224 6299 Ewan Kelly: [email protected] / 01 224 6269 |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]