|

Back to Blog

ECB confident it can create a digital euro. With ECB officials concerned that the Chinese central bank is potentially a couple of years away from launching its own digital renminbi after it conducted large-scale experiments, it has identified several scenarios that would require it to launch a digital euro. Two scenarios are:

Either way, some serious #regtech and #suptech will be required. Despite a 55-PAGE REPORT, the question is whether the ECB can stay ahead of the rapidly changing world of #digitalcurrencies and #payments. Central bankers are increasingly interested in the relatively new world of digital currencies, particularly since Facebook announced a plan to launch one called Libra that has the potential to overhaul the way money works. ECB officials believe the Chinese central bank is potentially a couple of years ‘ away from launching its own digital renminbi after it conducted large-scale experiments. In an interesting development, Bloomberg reported on 1 October 2020, that the European Central Bank has applied to trademark the term “digital euro” as officials prepare to release an assessment of the benefits and drawbacks of creating a digital version of the currency. The application was filed on 22 September by the ECB’s legal representatives Bock Legal, according to the website of the European Union Intellectual Property Office. An ECB spokesman confirmed the filing. The ECB outlined potential scenarios “that would require the issuance of a digital euro”. These include higher demand for electronic payments that creates a greater need for a “risk-free digital means of payment”, as well as the potential that a cyber attack or pandemic disrupts the existing payment system and requires a digital euro to serve as a back-up. Another scenario is a further sharp drop in cash usage that leaves some people financially excluded. Finally, it examined the potential rapid adoption of other private or public digital currencies including those issued by foreign central banks that ‘could “threaten European financial, economic and, ultimately, political sovereignty”. The ECB said a digital euro “also poses challenges, but by following appropriate strategies in the design of the digital euro the Eurosystem can address these”. My Linkedin Post here Sources:

0 Comments

Back to Blog

[first posted by Fintech UK]

Panel: Has the crisis helped companies shift from being product-centric to customer centric, are they ready for consumer of 2021? What: Fintech Week Lithuania: Panel: Has the crisis helped companies shift from being product-centric to customer-centric, are they ready for consumer of 2021? When: Tuesday 16th June 2020. Start time 9:55am (Irish/UK time) / 11:55am (Lithuania time). Where: Online Event. Cost: Free Registration: See registration link at https://fintechuk.com/events/covid19-fintech-shift-from-product-to-customer-centric Details: Fintech UK's Peter Oakes* (Board Director at global fintech / payments business TransferMate) joins an excellent line up of fellow panel members Agnė Selemonaitė, Deputy CEO & Board Member at ConnectPay and Anastasija Oleinika, CEO of TWINO Group in a lively session moderated by Nick Price, Chief Executive of Bright Purple. *Peter is also founder of Fintech Ireland, US Fintech, Fintech Cyprus, leading fintech advisory firm CompliReg and a director of several regulated fintech companies including Susquehanna International, Optal Financial Europe and AWM Wealth Advisers)

Back to Blog

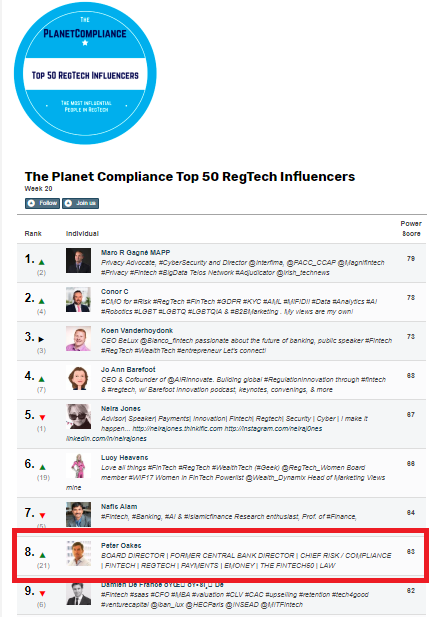

Yet again, our Peter Oakes, Non-Executive Director FinTech & FinServ and Founder of CompliReg and Fintech Ireland ranked in Top 10 of of the Top 50 RegTech Influencers. Planet Compliance updates a list of people that it finds are the key influencers in the field of RegTech. You'll find Peter Oakes featured almost every week in this list of RegTech influencers.

Peter was identified by the prestigious Chambers & Partners in January 2020 as leading band 1 FinTech advisor too.

Back to Blog

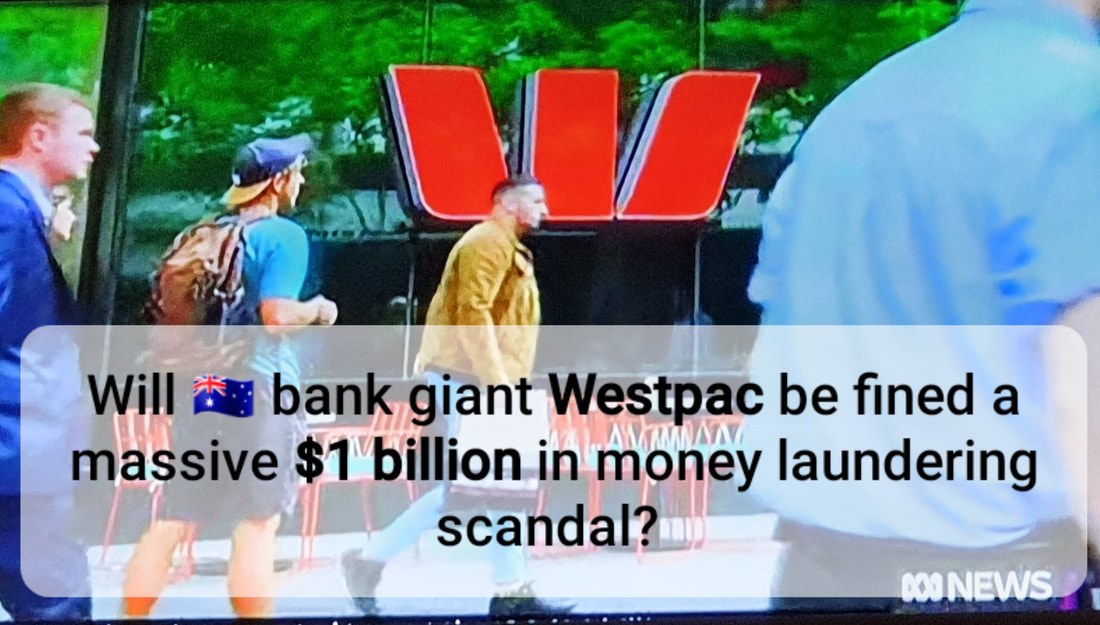

Australian Bank giant Westpac is expecting to fork out more than $1 billion as a result of its money laundering scandal and admitting to 23 million anti-money laundering breaches.

It's not just story about culture, conduct risk and financial crime risks. Far more importantly, it is a story of shame, leadership failure and financial pain for Westpac and relief for another Aussie bank. The fine would be the biggest corporate fine in Australian history. Westpac has revealed it expects the ongoing AUSTRAC investigation will cost it $1.03 billion. Such a fine will represent about 15% of the bank's 2019 profit. Shame: In November last year AUSTRAC, the entity responsible for preventing financial crimes, said the bank had violated anti-money laundering and counter-terrorism laws more than 23 million times (which the bank admits), allowing money tied to child exploitation in south-east Asia to flow freely. For example, Westpac's system was used by paedophiles to send money to the Philippines to pay for child abuse material without raising any red flags. Notwithstanding Westpac's admission, the bank is not going down without a fight. In the 57-page defence document filed with the court, Westpac denied AUSTRAC'S accusation that it failed to identify activity indicative of child exploitation risks. Leadership Failure: The scandal brought down Westpac's leadership, forcing the resignation of chief executive Brian Hartzer and the early retirement of chairman Lindsay Maxsted. Financial Pain: Last year Australian financial press reported that a penalty or settlement of $2 billion or $3 billion would see its CET1 ratio falling below 10.5% meaning the bank would be forced into another equity raising. And the trouble doesn't stop there for Westpac as the corporate regulator, ASIC, is probing into Westpac's previous $2.5 billion equity raise. Relief: Commonwealth Bank will be delighted to pass the mantle of the indignity of Australia's current money laundering record fine of $700 million to Westpac (Commonwealth Bank was fined for systemically failing to report around 54,000 suspicious transactions made through its "intelligent deposit machines"). If you want more on the story from the media, there are updates on an almost weekly basis - soon I guess daily basis. Just use this link to keep track of the story: "Westpac Austrac money laundering fine". And add case to your case studies and typologies in your AML / CTF training for everything from CDD, transaction monitoring, risk assessment, culture, condusct risk and (lack of) crisis management. Peter Oakes, Founder, CompliReg Peter Oakes is an experience anti-financial crime, fintech and board director professional. He served as Ireland's first Director of Enforcement and Financial Crime Supervision at the Central Bank of Ireland (2010-2013) in the aftermath of the financial crisis, leading the investigation and enforcement efforts into the Irish banking industry. Peter is a regular contributor to, and moderator and panel member at, ACAMS events.

Back to Blog

16 January 2020: Peter Oakes, Founder of CompliReg (and Founder of Fintech Ireland, Fintech UK, Fintech NI and US Fintech / USTechFin) has been recognised as a Leading Band 1 Consultant in Chambers & Partners’ 2020 Professional Advisers guide for FinTech – the premier ranking of professional advisers to the financial services industry.

Peter secured a nationwide Ireland Band 1 ranking – Chambers’ top-tier ranking – where it was noted that: Peter Oakes, who has vast international regulatory experience as a former director of the Central Bank of Ireland. A source says: ‘Peter is high-profile, he has very strong governance capabilities and is very good for a regulated FinTech company.' Peter is a non-executive director of regulated fintech companies in the payments, e-money and MiFID sectors and is an adviser and mentor to fintech and regtech startups and scaleups. In Ireland he is a consultant to Clark Hill and in the UK he is a consultant to Kerman & Co, which is supporting the Fintech UK project. Learn more about Peter Oakes’s rankings in the Chambers FinTech guide here: https://chambers.com/department/peter-oakes-consulting-fintech-49:2743:114:1:23173986 |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]