|

Back to Blog

Cohort #1 of Central Bank of Ireland’s Innovation Sandbox Programme: ‘Combatting Financial Crime’9/1/2025  Seven participants of the Central Bank of Ireland’s Innovation Sandbox Programme on ‘Combatting Financial Crime’ are: 1) AMLYZE is building an AML/CFT information-sharing framework that will use structured taxonomies and synthetic data to simplify detecting and preventing fraudulent activities. 2) Expleo Group has developed an anti-SMS fraud solution which installs on mobile phones to combat SMS fraud. 3) Forward Emphasis and Pasabi’s joint innovation will develop and test a Motor Insurance Application Fraud Analytics solution, leveraging AI-driven behavioural analytics, machine learning, and pattern recognition to detect fraud in the pre-sales process. 4) Roseman Labs enables secure, GDPR-compliant collaboration and analysis on sensitive data for regulated industries. 5) Sedicii (hello Rob Leslie) and PTSB Sedicii has partnered with PTSB to create a secure and private collaboration using zero knowledge proofs to verify names and addresses, in real-time, as part of their customer KYC process, using ESB Networks as the authority for address data in Ireland in full compliance with GDPR and which involves no sharing of personal data. 6) TrustElevate.com offers a privacy-preserving solution for verifying parental responsibility and child age. 7) Vidos.Id is developing digital identity verification solutions to help financial institutions verify digital identity documents and wallet-based credentials. There are many familiar names here and a couple we hadn't encountered at www.moneylaundering.ie and www.fintechireland.com. Since this all very serious hashtag#regtech, we better dust off the www.regtechireland.com website! All the best to the cohort. First posted here Combatting Financial Crime Theme The theme of the Innovation Sandbox Programme is: “Combatting Financial Crime – Through the use of innovative technology, foster and develop innovative solutions that minimise fraud, enhance KYC/AML/CFT frameworks, and improve day-to-day transaction security for consumers.” The programme will encourage collaboration across the ecosystem to support the fight against financial crime. Programme outputs will include inter alia the documentation and sharing of learnings in fraud prevention and detection. The programme also aims to facilitate the development of new ventures and new business models that solve challenges identified in this sandbox theme and facilitate the faster and safer deployment of substantially new technologies, products, or services. The Sandbox Programme framework comprises:

What is the Challenge?

What are the Problem Statements?

Read more here

0 Comments

Back to Blog

Received a letter from the Central Bank of Ireland's Anti-Money Laundering Division headed "AML Risk Evaluation Questionnaire (‘REQ’) Notification to [Name of Regulated Firm] (or ‘the firm’) to submit an REQ on an Annual Basis." last month with a return date this month? If so you are not alone.

The letter reminds that credit and financial institutions are required to have anti-money laundering (AML) and countering financing of terrorism (CFT) preventive measures to ensure compliance with the Criminal Justice (Money and Terrorist Financing) Acts 2010 to 2021, a well as reminding of the obligation to comply with EU Council Regulations setting out financial sanctions (‘FS’) measures. The CBI has established the REQ to seek information regarding individual firms’ exposure to Money Laundering / Terrorist Financing risks and also the AML/CFT compliance framework. Firms are being informed to submit the REQ in the specified format via the CBI's Online Reporting System on an ANNUAL BASIS within the time period specified on ONR. The CBI has informed firms that "for 2021, this deadline for the submission of the REQ return is 18 June 2021". Not only is the form detailed, and there are a few potential ways of interpreting some of the questions, or at least their interaction with other questions, but importantly for Boards of Directors note: i) Statement of Compliance: "... the REQ includes a statement to be signed by the firm confirming compliance with the firm’s AML/CFT/FS obligations. This statement if [sic] compliance should be signed and dated by a person who is duly authorised to do so by the Board (or equivalent). Ideally this person will have responsibility for AML/CFT/FS within the firm." NB this person doesn't need to be in a PCF role, but the CBI expect them to be of sufficient seniority within the firm to provide the confirmation sought. ii) Record Retention: "A record of the person who signed the statement of compliance must be formally noted in the Board minutes (or equivalent) when it is brought forward for consideration. The original signed and dated hard copy of the statement of compliance and the accompanying REQ is required to be kept on file and made available for review by the Central Bank on request." Need assistance with your risk assessment? Get in contact with us at the details here. Further reading: Risk Evaluation Questionnaire ('REQ') Return Building upon the obligations of credit and financial institutions under the CJA 2010, the Central Bank has developed a REQ in order to seek information regarding individual firms' exposure to ML / TF risks and also their AML / CFT compliance framework. Firms selected by the Central Bank to submit an REQ are required to submit the REQ in the specified format, through the Central Bank's Online Reporting System ('ONR'), within the time period specified on ONR. The minimum frequency that a firm will be required to submit an REQ is predicated on the level of ML/TF risk presented by the firm, either by virtue of its business model and/or the sector into which it falls (for further information on the frequency of submission please see the Table: AML/CFT Minimum Supervisory Engagement Model on the Central Bank AML / CFT Supervision Tab).

Linkedin Post: https://www.linkedin.com/posts/peteroakes_antimoney-aml-cft-activity-6808437129467756546-vRba

Back to Blog

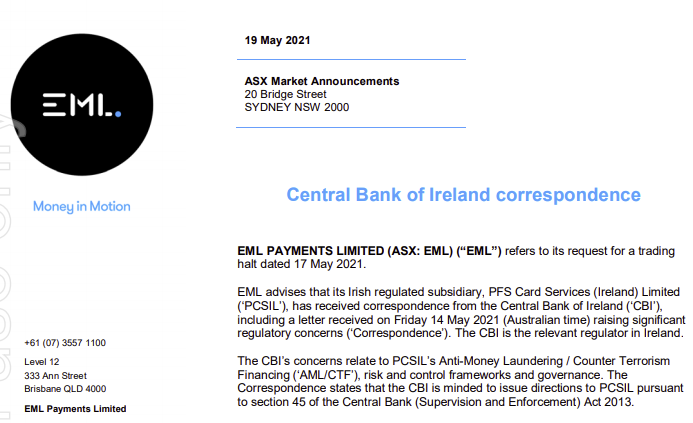

The ASX Market Announcement says:

"EML PAYMENTS LIMITED (ASX: EML) ("EMU') refers to its request for a trading halt dated 17 May 2021. EML advises that its Irish regulated subsidiary, PFS Card Services (Ireland) Limited ('PCSIL'), has received correspondence from the Central Bank of Ireland ('CBI'), including a letter received on Friday 14 May 2021 (Australian time) raising significant regulatory concerns ('Correspondence'). The CBI is the relevant regulator in Ireland. The CBI's concerns relate to PCSIL's Anti-Money Laundering / Counter Terrorism Financing ('AML/CTF'), risk and control frameworks and governance. The Correspondence states that the CBI is minded to issue directions to PCSIL pursuant to section 45 of the Central Bank (Supervision and Enforcement) Act 2013. The Correspondence does not concern EML's Australian or North American operations, or the operations of PFS' UK subsidiary ('Prepaid Financial Services Limited' which is incorporated in England and regulated by the FCA), or EML's other Irish regulated subsidiary ('EML Money DAC')." ASX Announcement in PDF and at source.

Back to Blog

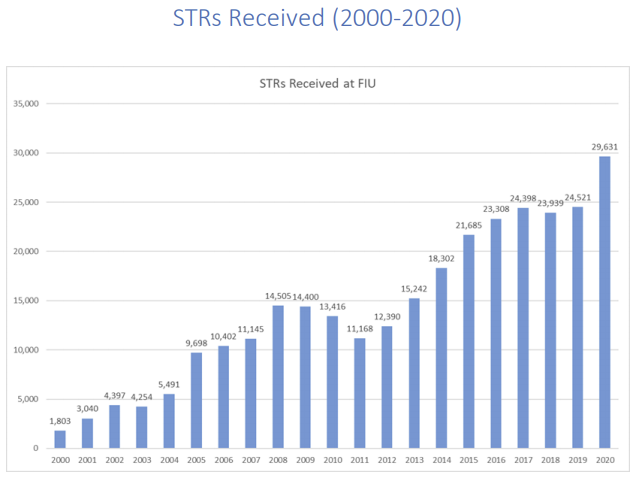

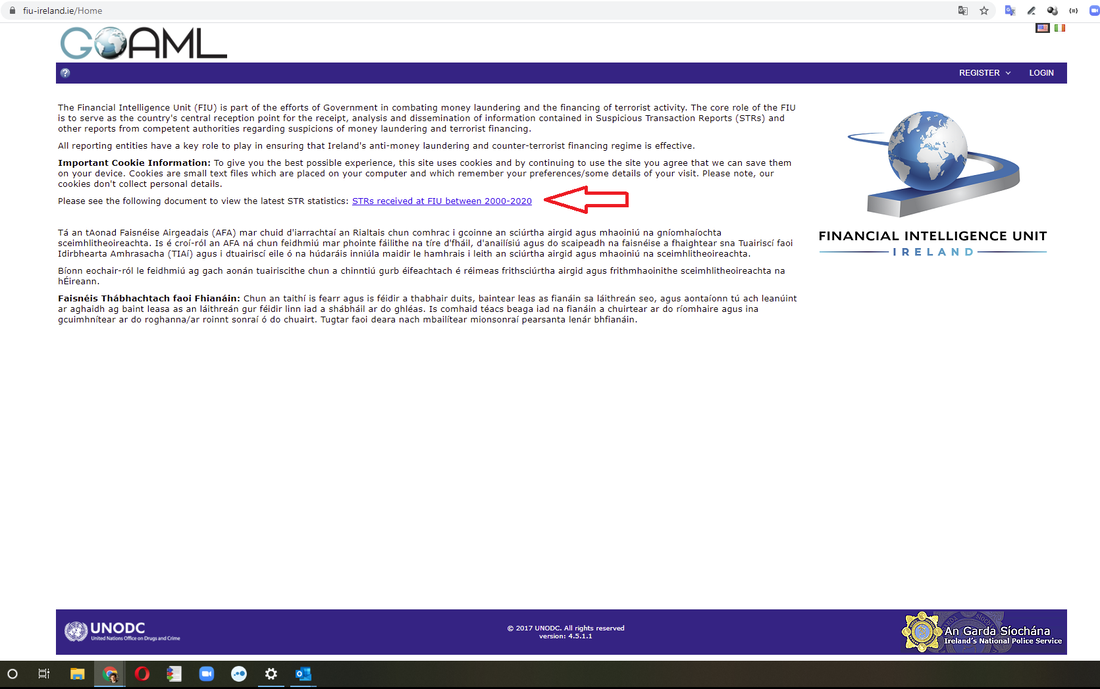

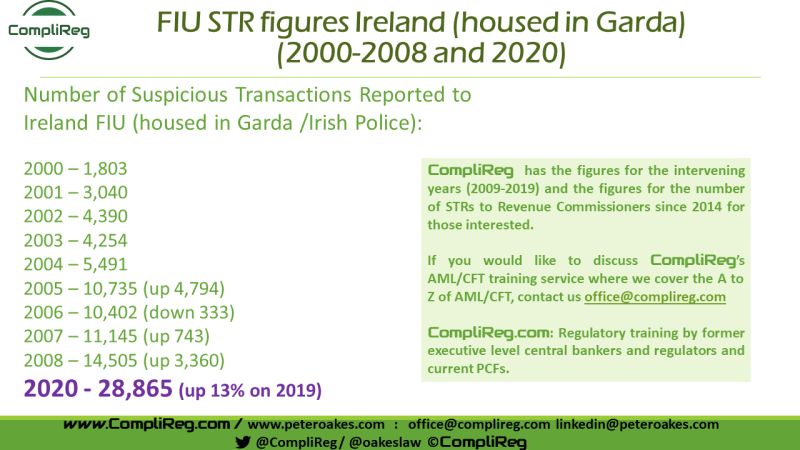

Source: 11/05/2021 https://fiu-ireland.ie/Home (see screenshots & link to report in blog) Less than a week ago there was no readily accessible and publicly available data (in one spot) for historic figures on the number of money laundering suspicious transaction reports in Ireland. To assist my GRC network which ask me regularly about such data, I put out a few posts on Linkedin, including this one - https://bit.ly/3o8JvCt. I received some responses and comments politely querying the accuracy of my figures. In reply I posted the underlying sources, being the Garda (Irish Police) / FIU Ireland and Financial Action task force. At the time, the only available data for 2020 was by journalist Conor Lally, at the Irish Times in his article of 4 May 2021. Jump forward to today (or perhaps it was yesterday as there is no date), the Financial Intelligence Unit in Ireland published the above image and a three (3) page report providing details on STRs Received (2000-2020). If you visit that site and the data does not appear, no problem, I have uploaded the file here.

I am glad to see that my data and that of the FIU matches for the years 2000, 2001, 2003 & 2004. For 2002 I have 4,390 v FIU figure of 4,397 and in for 2005 I have 10,735 v FIU figure of 9,698 (hardly material). Still I find this strange as my figures were sourced from Garda & FATF reports at the time. When I published the 2020 figure of 28,865, that was based on the above Irish Times article which was published at least 10 days before the FIU publication which reported 29,631 (2.5% difference - or a rounding error!).

Thanks to Steven Meighan for his LinkedIN post yesterday (11 May 2021) and previous engagement on money laundering STRs. A good thing about Linkedin is that it gets people engaged & often leads to great outcomes, like the publishing by the FIU / Garda of such comprehensive data for the first time in one consolidated document and easily accessible. We all now have an agreed historical set of facts and figures, and given it is published by FIU Ireland, it's official data.  Other areas of the FIU release which caught my eye are:

Back to Blog

“The EBA recalls that a proper risk assessment must include such considerations and cannot be a blind instrument used to get rid of risky clients,” Peter Oakes, former director of enforcement and AML at the Central Bank of Ireland, European Union, United Kingdom May 11 2021 by Gabriel Vedrenne, ACAMS

Banks and national regulators should adopt a more finely tuned, risk-based approach towards compliance and supervision to prevent the wholesale offloading of money services businesses and other categories of clients they view as inherently prone to illicit finance. After publishing more than 400 pages of guidance this month to help financial institutions adopt a more nuanced system for evaluating financial crime-related risk, the European Banking Authority clarified Monday that its intent was to combat the now decade-long de-risking phenomenon, not exacerbate it. “De-risking can be a legitimate risk management tool in some cases but it can also be a sign of ineffective ML/TF [money laundering and terrorist financing] risk management, with severe consequences,” the EBA said Monday. “It has become apparent that more comprehensive action is needed to address unwarranted de-risking.” Since the beginning of March, the EBA has listed the threats of money laundering and other crimes affecting the European Union, issued new guidelines on key aspects of risk-based compliance and formally requested feedback on future guidance for risk-based supervision. Nonprofit groups, especially those in warzones, and asylum seekers without standard due-diligence records, often lack financial services, but the impact of de-risking is much broader, the EBA claimed Monday. MSBs and other cash-intensive businesses also suffer from overly cautious banks, as do firms whose products facilitate anonymity, such as prepaid card providers. Real estate companies struggle to open and maintain bank accounts, according to the EBA, as do cryptocurrency exchanges, e-money issuers and other firms in emerging sectors that banks perceive as having limited knowledge of anti-money laundering compliance. “The EBA recalls that a proper risk assessment must include such considerations and cannot be a blind instrument used to get rid of risky clients,” Peter Oakes, former director of enforcement and AML at the Central Bank of Ireland, told ACAMS moneylaundering.com after reviewing Monday’s statement. “Financial institutions must be prepared to answer questions about it.” Many banks in Europe have grown reluctant to handle the transactions that back remittances to the world’s poorest countries, and now even hesitate to serve real estate agents, soccer clubs, corporate services providers and other parties whose risks they consider unmanageable. De-risking has also reached U.S. financial institutions and drawn the attention of the Treasury Department’s Financial Crimes Enforcement Network, which encouraged banks in guidance seven years ago to rethink any decision to shun the remittance industry. “The Bank Secrecy Act does not require, and neither does FinCEN expect, banking institutions to serve as the de-facto regulator of the money services business industry any more than of any other industry,” FinCEN advised in 2014. “It is not possible for a bank to detect and report all potentially illicit transactions that flow through an institution.“ Reputations to consider A mindset of corporate social responsibility has also led to the termination of accounts and services for companies in industries perceived as risky “from an environmental, security or health perspective,” such as tobacco, weapons and coal. According to the EBA, this trend has had the perverse effect of encouraging rejected clients to turn to institutions in jurisdictions with lax AML supervision, or worse, to underground banks and other informal channels that operate beyond government supervision. “The risk associated with individual business relationships may vary, even within one category,” the EBA warned Monday. “The application of a risk-based approach … does not require financial institutions to refuse, or terminate, business relationships with entire categories of customers that are considered to present higher ML/TF risk.” National regulators should address the trend by improving their grasp of sectoral risks, and pay more attention to the affected industries to restore the trust of banks, the EBA recommended. “This may include increased supervisory activities in the sector or additional guidance to the sector,” the regulator suggested. “Furthermore, the EBA encourages competent authorities that have not yet performed an assessment of de-risking in their jurisdictions to consider performing such an assessment.” Several national regulators, including France’s Prudential Supervision and Resolution Authority and Britain’s Financial Conduct Authority, have sought to address de-risking through guidance, public statements and technology. Since 2011, the Central Bank of Ireland has collected more data on the operational risks of affected businesses through its “Probability Risk and Impact SysteM,” or PRISM, and by requiring financial technology-centric firms, also known as fintechs, to provide more details on their business models than other regulated institutions. But the extent of de-risking varies greatly across Europe, said Oakes, now a consultant in Dublin. “Data is the key, and not everyone collects and analyzes the same amount at the same level,” Oakes said. “As EU institutions operate within a framework aimed at reducing regulatory arbitrage and supervisory divergence, it is only a matter of time before uniform operational rules emerge for the entire bloc, even more with regards to the plan to create an EU-wide supervisor.” In the interim, the EBA encouraged banks to find a path to engage with high-risk clients, such as by adjusting the level and intensity with which they monitor them, or by offering them only basic financial products and services to reduce their exposure to financial crime. De-risking has also appeared on the agenda of the Financial Action Task Force, which sets global AML standards. The intergovernmental group launched an initiative last month to study and mitigate the consequences of incorrect implementation of its recommendations for a risk-based approach. Source: https://www.lexology.com/library/detail.aspx?g=4e1d9412-d4d5-475d-8cbf-ca0c0fcf4681 See also - https://www.lexology.com/library/detail.aspx?g=eef962ad-80bc-43ed-aece-5c19595ad4a9

Back to Blog

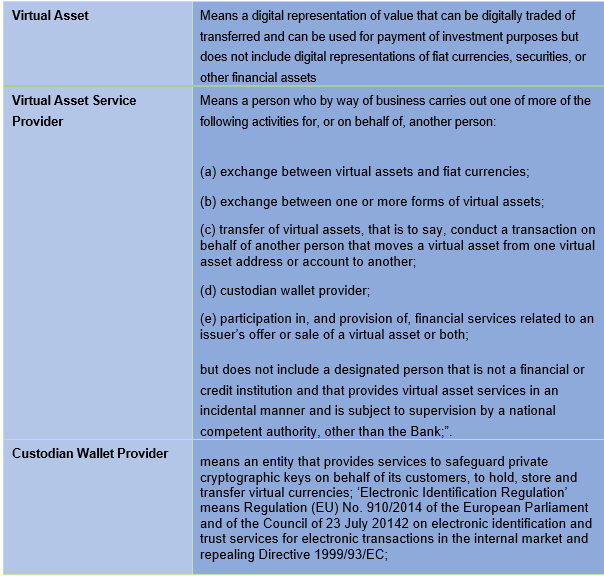

Stephen Fletcher, Consultant, CompliReg Stephen Fletcher, Consultant, CompliReg Summary Virtual Asset Service Providers (VASPs) operating in Ireland now need to demonstrate that they are compliant with the provisions of the 5th Money Laundering Directive (AMLD5) which recently came into effect on Friday 23rd April 2021. Preceding that date CompliReg, together with Fintech Ireland, hosted a webinar for VASPs, e-money and payments firms. Details of that event here. Given the demand from the audience, CompliReg and Fintech Ireland are hosting another Roundtable on the topic on Thursday 6th May - ROUNDTABLE: So, you want to be a Virtual Asset Service Provider? Background AMLD5 aims to remove the anonymity from the process of providing virtual asset based services. This applies to any organisation which provides exchange services between fiat and virtual currencies, as well between virtual assets or custodian wallet providers; bringing them into the scope of the EU’s anti-money laundering and counter-terrorist financing (‘AML/CFT’) framework. The 2021 Act The Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2021 (the "Act") amends the current Irish AML/CTF legislation, which started life a decade ago through the Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 (as amended). New Definitions relating to Virtual Assets The Act contains the following new definitions:  Designated Persons

The Act brings VASPs within the meaning of "designated person" (equivalent to an "obliged entity" under EU anti-money laundering law). The relevant obligations (Relevant Obligations) of designated persons under the Irish AML regime can be summarised as follows:

Requirement to Register The Act requires that a person shall not carry-on business as a Virtual Asset Service Provider unless the person has successfully registered with the Central Bank of Ireland (Central Bank). This is a registration for AML/CFT purposes only. A firm currently authorised by the Central Bank under a different regime which is also acting as a Virtual Asset Service Provider will still be required to register as a VASP. Whilst there is a three-month transitional period for VASPs to conclude the registration process the Act, which commenced operation on Friday 23rd April (commencement date), other than section 8 of the Act which commenced on Saturday 24th April, applies as of the commencement date. This means that regardless of an existing VASP having three months to register, the VASP must comply with the Act on and from the commencement date. This means that VASPs availing of the transition period must comply on and from 23rd April with the Relevant Obligations listed above. The Act sets out the high-level details of the registration process, and the grounds under which the Central Bank may refuse to register a VASP. These grounds include:

Preparation The Central Bank’s website contains useful information for those requiring registration as a VASP, including the Criminal Justice Act* (as at commencement date), Guidelines on Fitness & Probity of Principal Officers/Beneficial Owners, and links to the AML/CFT Registration Form. The Central Bank will not accept a registration application until the applicant has been through the pre-registration and has obtained a Central Bank Institution Number. The Central Bank has also indicated that its current graduated approach to AML/CFT supervision will apply equally to VASPs, meaning that firms which present a higher risk of money laundering and/or terrorist financing will be subject to higher intensity and intrusive supervisory measures than those presenting a lower risk. Next Steps As many VASPs shall become designated persons for the first time, they should review their AML/CTF frameworks, their Relevant Obligations, legislation and guidance now. Given that the Act has now commenced in operation, applicants should submit a Pre-Registration Information Form to the Central Bank to request a Central Bank Institution Number as soon as possible. Being within the AML/CTF framework will surely bring benefits such as greater confidence to end-users (i.e., customers – individuals and corporates) of VASPs and hopefully, more banking partners will consider opening up their services to VASPs particularly ahead of the proposed Markets in Crypto Assets Regulation 2020/0265. Support Available As with any new process, it can appear complex and daunting until you have been through it a few times. Thankfully help is at hand through CompliReg. If you would like to setup an initial discussion to discuss your requirements, please check out our page and complete the enquiry form at https://complireg.com/vasp.html. Stephen Fletcher or Peter Oakes will get back to you ASAP. Our details at https://complireg.com/team.html. This document (and any information accessed through links in this document) is for guidance purposes only and does not constitute legal advice. CompliReg does not provide legal services. Where legal services are required, CompliReg works with a select number of law firms. If you are a law firm and wish to be considered for our panel, please contact [email protected].

Back to Blog

* UPDATE: In response to emails I've uploaded a slideshow of our consolidation - available here. Clients will receive a free amendable/searchable copy *

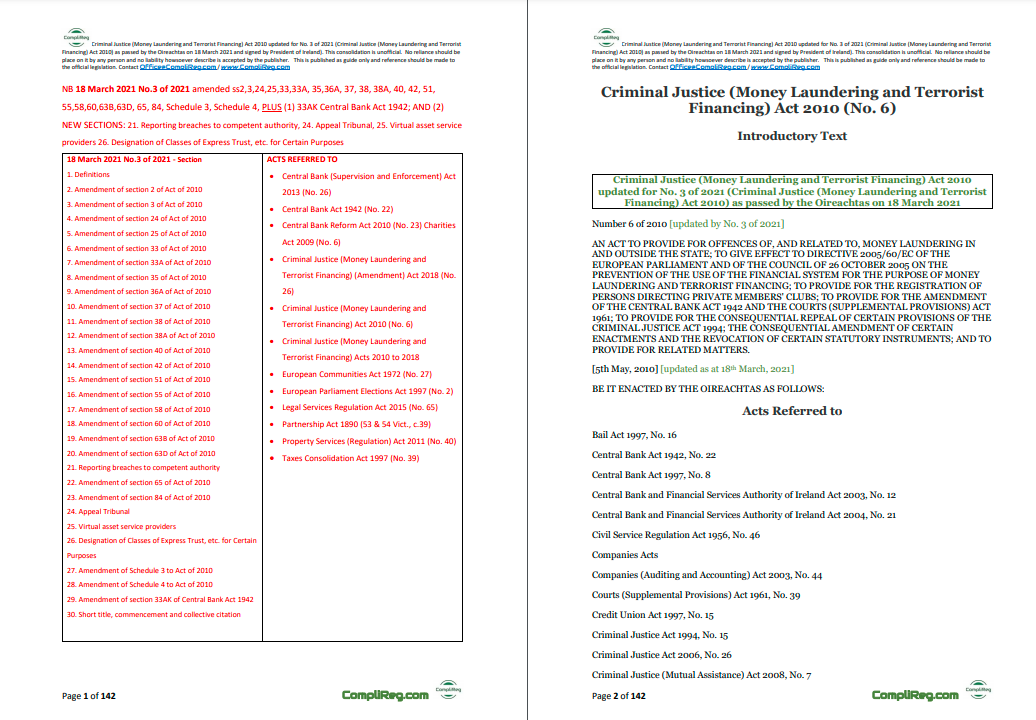

Comments on the updated Irish #moneylaundering & #terroristfinancing legislation. What: Ireland signed into law the Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2021 (the “2021 Act”). The 2021 Act (No. 3 of 2021) makes a number of changes to the 2010 Act (No. 6 of 2010) When: 18 March 2021. Legislation passed by Oireachtas (signed into Law by the President of Ireland). The 2021 Act takes effect on Friday 23 April 2021 with remaining legal provisions taking effect on the following day (23 April 2021). A copy of the commencement order is available here. Action: Time to update your #Compliance & #FinancialCrime Risk Frameworks, Risk Assessments, Policies, Manuals & Procedures. What areas of the 2010 Act are impacted that you need to know and take into account to update your compliance documents? See the comments section below where I've listed the areas from the 2010 Act impacted by the 2021 Act. How: Contact the team at CompliReg. We are undertaking several reviews of policies, procedures and manuals in light of the recent changes made to Irish AML/CTF law. We have tracked the changes in our consolidation of the 2010 Act up until and including Act No 3 of 2021. Contact the team at [email protected] with your business contact details for a discussion of a review. Further Reading: Money Laundering - Amendments to implement 5th AMLD into Ireland (18 March 2021)

Back to Blog

Peter Oakes, Founder, Complireg Peter Oakes, Founder, Complireg UPDATE: The law commenced operation on Friday 23rd April 2021. See Stephen Fletcher's blog of Saturday 1 May 2021 for further details Below is my linkedin post of 16 April 2021. I have been asked to put a copy of the consolidation online. We spent a lot of time preparing the consolidation and are happy to share the below slideshow. If you would like a copy of the document in pdf which you can copy, paste and search within, please email [email protected] and we will inform of the costs and email. "Some comments on the updated Irish #moneylaundering and #terroristfinancing legislation. Linkedin Post: What: Ireland signed into law the Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2021 (the “2021 Act”). The 2021 Act (No. 3 of 2021) makes a number of changes to the 2010 Act (No. 6 of 2010) When: 18 March 2021. Legislation passed by Oireachtas & signed into Law by the President of Ireland Action: It’s time to update your #Compliance & #FinancialCrime Risk Frameworks, Risk Assessments, Policies, Manuals & Procedures. So what areas of the the 2010 Act impacted by the changes in March do you need to know and consider taking into account to update your compliance documents? See the comments section below where I've listed the areas from the 2010 Act impacted by the 2021 Act. How: Contact the team at CompliReg. We are undertaking several reviews of policies, procedures and manuals in light of the recent changes made to Irish AML/CTF law. We have tracked the changes in our consolidation of the 2010 Act up until and including Act No 3 of 2021. Contact the team at [email protected] with your business contact details for a discussion of a review. We'll be sending a copy of our up-to-date consolidated version of the 2010 Act to our clients this week." Post at https://www.linkedin.com/feed/update/urn:li:activity:6788600737791303680/

Back to Blog

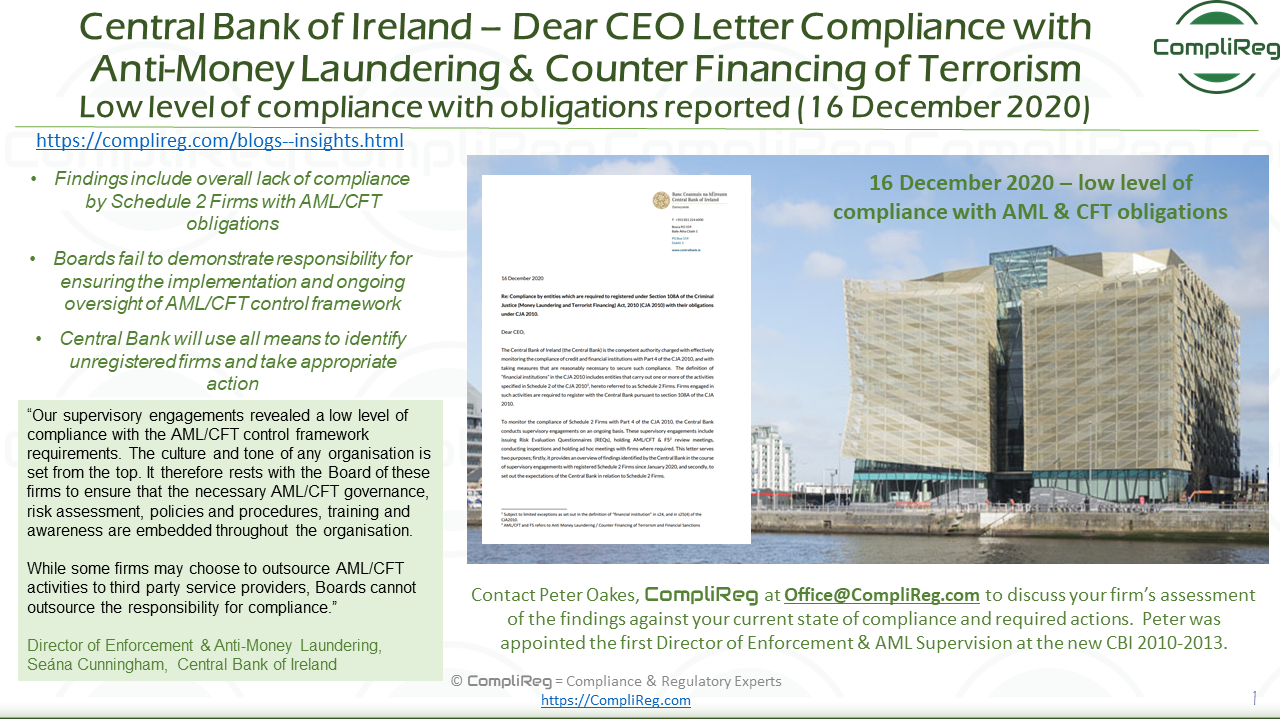

Central Bank publishes “Dear CEO” letter to Schedule 2 firms on low level of compliance with Anti-Money Laundering and Counter Financing of Terrorism obligations

The Central Bank has today (16 December 2020) published the outcome of supervisory engagements undertaken in respect of Schedule 2 Firms to assess compliance with their obligations under Criminal Justice (Money Laundering and Terrorist Financing) Act 2010 (CJA 2010). The "Dear CEO" letter*, outlines the Central Bank’s expectations of firms in relation to Anti-Money Laundering/Counter Financing of Terrorism (AML/CFT) and Financial Sanctions (FS) requirements and details follow-up actions to be taken by CEOs and Boards in response to the findings outlined. The examination, which comprised of both inspections and review meetings, found an overall lack of compliance across all areas of the AML/CFT control framework. There is also poor understanding of the requirements from Board and senior management levels, including at those firms who outsourced their AML/CFT and FS activities to third parties. The examination identified a number of failings across Schedule 2 Firms, including:

Director of Enforcement & Anti-Money Laundering, Seána Cunningham said: “The Central Bank expects all firms to be alert to the risks that money laundering and criminal financial activities may pose to their customers and business, and the wider integrity of the Irish financial system. This requires CEOs and Boards to have in-depth knowledge and understanding of their Anti-Money Laundering and Counter Financing of Terrorism obligations. It is also essential to have the necessary control framework in place to ensure protection of their business and customers. “Our supervisory engagements revealed a low level of compliance with the AML/CFT control framework requirements. The culture and tone of any organisation is set from the top. It therefore rests with the Board of these firms to ensure that the necessary AML/CFT governance, risk assessment, policies and procedures, training and awareness are embedded throughout the organisation. While some firms may choose to outsource AML/CFT activities to third party service providers, Boards cannot outsource the responsibility for compliance. “We will continue to engage directly with those firms where compliance weaknesses and failures have been identified to ensure that they are addressed. We also require all firms to review the content of this letter to ensure that they assess their own compliance with the issues identified. “We are also taking this opportunity to remind all firms to assess their activities to determine if they are required to register with us under Schedule 2. Firms who fail to register are at risk of significant criminal and/or administrative sanctions. In 2021, the Central Bank will use all means available to identify those firms not registered and take appropriate action.” ENDS Notes to Editor

Further information Media Relations: [email protected] / 01 224 6299 Ewan Kelly: [email protected] / 01 224 6269

Back to Blog

Here's one for the #moneylaundering typology case studies for #MLROs as part of regulatory training requirements!

Relates to the collapse of major investigation into the Kinahan cartel and more than half a billion euros- particularly €500,000,000 stash of cars, properties & cash handed back to the accused by a Spanish judge after collapse of money laundering case. Can understand that staff and MLROs at financial institutions and other obliged entities which do a lot of the initial legwork in identifying suspicious transactions may feel underwhelmed (to say the least) when a case like this collapses. We should train on all types of cases, regardless if there is a criminal outcome or not. Staff (and boards) need to appreciate that not all suspicious transactions reports will 'result' in a criminal outcome, but that doesn't excuse obliged entities and their staff from complying with the legal requirement to report suspicious transactions. A skill MLROs and trainers need to focus upon is motivating staff, themselves and the senior executive to stay the course. https://www.linkedin.com/posts/peteroakes_moneylaundering-mlros-financialcrime-activity-6719937607700135936-jZUH #antimoneylaundering #financialcrime #mlros #suspicioustransactions #lawenforcement Check out the linkedin post with link to news article. |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]