|

Back to Blog

Peter Oakes, Enforcement Expert & Lawyer Peter Oakes, Enforcement Expert & Lawyer Here's an enforcement action which will serve as a useful typology for fitness and probity, not to mention culture and behavior, as Ireland heads towards a Senior Executive Accountability Regime by Peter Oakes Peter is was appointed the first Director of Enforcement and Ant-Money Laundering at the newly reconstituted Central Bank of Ireland in 2010, where he led and developed the creation and staffing of the new Enforcement and Anti-Money Laundering Directorate with responsibility for delivering administrative sanction procedure enforcement actions, unauthorised providers actions, fitness and probity supervisory and enforcement actions and development of new regulatory laws. Peter has worked on a number of regulatory enforcement matters since leaving the Central Bank and is available to advise and represent on such matters. Read more here. Bullet Point Summary

Enforcement Action Notice: Mr Rory O’Connor, former Executive Director and Chief Financial Officer of RSA Ireland Insurance DAC (RSAII) disqualified for 8 years 4 months and fined €70,000 by the Central Bank of Ireland for his admitted participation in a breach of financial services law by RSAII On 9 June 2020, the Central Bank of Ireland (the Central Bank) reprimanded Mr O’Connor, disqualified him from being a person concerned in the management of a regulated financial service provider for a period of 8 years 4 months, and imposed a fine of €70,000 for his admitted participation in RSAII’s failure to maintain sufficient technical reserves from February 2010 to 30 September 2013 (the Relevant Period). This enforcement action against Mr O’Connor follows a separate investigation conducted by the Central Bank in respect of RSAII, at the conclusion of which the Central Bank reprimanded RSAII and imposed a financial penalty of €3.5 million in December 2018. [footnote 1] The Central Bank’s investigation in respect of RSAII found that deliberate and wrongful under-reserving of large loss claim reserve estimates resulted in incomplete and inaccurate information being relied upon in the calculation of RSAII’s technical reserves. The investigation found that the claim reserve estimates on RSAII’s claims database were understated in the sum of approximately €29 million as at 30 September 2013. The Central Bank’s investigation in respect of Mr O’Connor, who held the positions of Executive Director and Chief Financial Officer (CFO) in RSAII, found that he knowingly and actively participated in RSAII’s failure to maintain sufficient technical reserves through his involvement in the under-reserving of large loss claim reserve estimates. In particular, Mr O’Connor:

Following a full investigation, the Central Bank determined that Mr O’ Connor’s misconduct merited a disqualification period of 12 years and a monetary penalty of €100,000. In accordance with the settlement discount scheme provided for in the Central Bank’s Administrative Sanctions Procedure, these sanctions were reduced to 8 years 4 months and €70,000 respectively. The Central Bank’s Director of Enforcement and Anti-Money Laundering, Seána Cunningham, stated: “The Central Bank takes enforcement action against senior individuals in regulated financial services firms in order to hold them accountable where they have participated in serious or significant breaches of regulatory requirements. For over three and a half years, in his roles as Chief Financial Officer and Executive Director on the board of RSAII, Mr O’Connor knowingly participated in the systematic under-reserving of large loss claims, actively facilitated the on-going operation of the under-reserving and concealed it from the Central Bank through the provision of inaccurate financial information. The under-reserving of large loss claim reserve estimates directly contributed to the understatement of RSAII’s technical reserves and resulted in the Firm’s financial position being artificially enhanced. The failure to maintain adequate technical reserves led to significant risk for policyholders in the event that RSAII did not hold sufficient assets to meet its liabilities and was, as a result, unable to pay claims made against and by its policyholders. Mr O’Connor’s conduct in this case was deliberate and fell far below the standards expected of him in the roles he held in RSAII. It is imperative that individuals working in regulated financial services and particularly those in senior roles, fully understand the risks and consequences that their decisions, actions and behaviours may have for an organisation, its employees, its customers and the wider market. By taking action to address misconduct in the regulated financial services sector, the Central Bank seeks to safeguard financial stability and ensure that consumers and financial markets are protected from wrongdoing and that misconduct within the regulated financial services sector is deterred. It also signals to the market, the practices and behaviours, of those in senior roles in financial services, that will not be tolerated and highlights the serious consequences should an individual fail in such a material and deliberate way to comply with regulatory requirements. The sanctions imposed on Mr O’Connor reflect the nature and seriousness of his actions in this case.” ADMITTED PRESCRIBED CONTRAVENTION Enforcement Action against RSAII RSAII is an insurance undertaking authorised and regulated by the Central Bank. Mr O’Connor was an Executive Director and Chief Financial Officer of RSAII from 2010 to 2013. On 18 December 2018, the Central Bank reprimanded and imposed a fine of €5,000,000 on RSAII which was reduced to €3,500,000 with the application of the settlement discount scheme in respect of serious breaches of financial services law (admitted by RSAII), including but not limited to the failure to establish and maintain technical reserves in accordance with Article 13(1)(a) of the European Communities (Non-Life Insurance) Framework Regulations 1994, S.I. No. 359 of 1994 (the 1994 Regulations). Technical reserves are the amount set aside by an insurance company to cover its liability for claims. Mr O’Connor’s Participation in the Prescribed Contravention Mr O’Connor has admitted his participation in the prescribed contravention in RSAII’s breach of Article 13(1)(a) of the 1994 Regulations, which requires an insurance undertaking to maintain sufficient levels of Technical Reserves (the Prescribed Contravention). The Central Bank’s investigation found that Mr O’Connor participated in the Prescribed Contravention through his involvement in the deliberate manipulation of large loss claim reserve estimates, referred to in the enforcement action against RSAII as the “Under-Reserving Process”. As a result of the Under-Reserving Process, specific large loss claims were deliberately suppressed by significantly delaying the recording of the reserve estimates recommended by RSAII’s claims handlers (the Recommended Estimates) in the claims database and/or by recording claim reserve estimates which were lower than the Recommended Estimates. To give a clear example of how the Under-Reserving Process operated in practice, a claim relating to a serious motor accident should have been recorded on RSAII’s claims database with a recommended estimate of €2.7 million. However, the claim was in fact recorded with a claim reserve estimate of just €20,001 thus, making RSAII’s potential liability for that claim appear to be far less than it was. Mr O’Connor has admitted his involvement in the Under-Reserving Process as follows: During the Relevant Period, Mr O’Connor participated in frequent, undocumented meetings, during which claim reserve estimates for large loss claims were deliberately and wrongfully manipulated resulting in the relevant claim reserve estimates being understated on the Firm’s official claims database. From around 2012 onwards, Mr O’Connor became more involved in the under-reserving by assuming responsibility for communicating the outcome of the meetings and the decisions made in relation to the understated claims to RSAII’s Claims Department together with the claim reserve estimate amounts which could be officially recorded on the claims database. Specific large loss claims were deliberately suppressed by significantly delaying the recording of the Recommended Estimates in the claims database and/or by recording claim reserve estimates which were lower than the Recommended Estimates. This was referred to in the Enforcement Action against RSAII as the “Under-Reserving Process”. The under-reserving was concealed by from the Central Bank the presentation and provision of inaccurate and misleading financial information. The Central Bank’s investigation found that Mr O’Connor intentionally concealed the Under-Reserving Process in the following ways:

The Impact of the Under-Reserving Process on the Technical Reserves Claim reserve estimates are used in the calculation of technical reserves. The Under-Reserving Process resulted in the claim reserve estimates for certain large loss claims being significantly understated on RSAII’s claims database and consequently the claim reserve estimates on the database did not accurately reflect the estimated cost of these claims. As at 30 September 2013, the systematic under-reserving of large loss claims resulted in claim reserve estimates for seventeen large loss claims being recorded on RSAII’s claims database in amounts significantly lower than the Recommended Estimates. The shortfall between the claim estimates recorded on RSAII’s claims database and the Recommended Estimates was €29,300,070, as at 30 September 2013. Ultimately, as a result of the Under-Reserving Process, RSAII was required to increase its technical reserves as at 30 September 2013 to take account of these under-reserved large loss claims, requiring a significant capital injection from RSA Insurance Group PLC. On the basis that a decrease in technical reserves has the effect of decreasing an insurer’s technical expenses and thus increasing the amount that the Firm could report as profit, the under-reserving also resulted in the artificial inflation of the Firm’s profits for 2012. SANCTIONING FACTORS In determining the appropriate sanction, the Central Bank has considered the guidance on the sanctioning factors set out in Part II of the ASP Sanctions Guidance (November 2019). The following factors are relevant in this case: The Nature, Seriousness and Impact of the Contravention

Mr O’ Connor’s conduct after the contravention Mitigating

Mr O’Connor’s previous record Mitigating:

Other Considerations

This settlement represents the conclusion of the Central Bank’s investigation into Mr O’Connor. NOTES

[1] Central Bank of Ireland Enforcement Action Notice December 2018

0 Comments

Back to Blog

[first posted by Fintech UK]

Panel: Has the crisis helped companies shift from being product-centric to customer centric, are they ready for consumer of 2021? What: Fintech Week Lithuania: Panel: Has the crisis helped companies shift from being product-centric to customer-centric, are they ready for consumer of 2021? When: Tuesday 16th June 2020. Start time 9:55am (Irish/UK time) / 11:55am (Lithuania time). Where: Online Event. Cost: Free Registration: See registration link at https://fintechuk.com/events/covid19-fintech-shift-from-product-to-customer-centric Details: Fintech UK's Peter Oakes* (Board Director at global fintech / payments business TransferMate) joins an excellent line up of fellow panel members Agnė Selemonaitė, Deputy CEO & Board Member at ConnectPay and Anastasija Oleinika, CEO of TWINO Group in a lively session moderated by Nick Price, Chief Executive of Bright Purple. *Peter is also founder of Fintech Ireland, US Fintech, Fintech Cyprus, leading fintech advisory firm CompliReg and a director of several regulated fintech companies including Susquehanna International, Optal Financial Europe and AWM Wealth Advisers)

Back to Blog

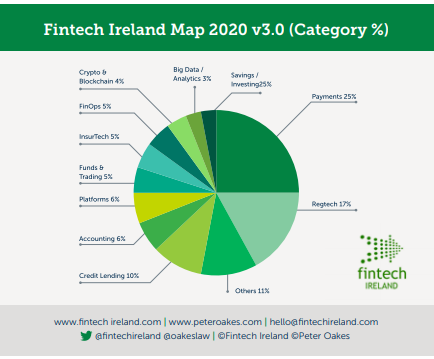

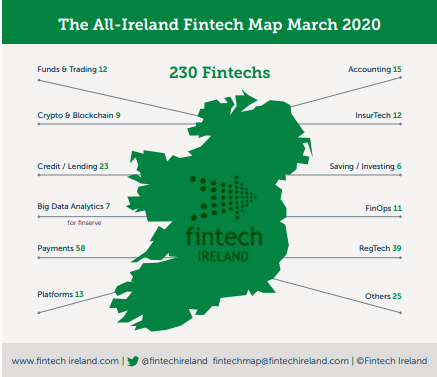

"As I write, the impact on people and businesses arising from the coronavirus is being felt across all parts of society and the economy. It is keeping many of us exceptionally busy not only assisting our clients but dealing with the impacts on our businesses too." Fintech Ireland's and CompliReg's Peter Oakes writes on the The Irish Fintech Ecosystem: Headwinds and Tailwinds (and the Making of a Global Fintech Centre) for CPA Ireland's Accountancy Plus Download the article in PDF and visit CPA Ireland's excellent resources. Continue reading below. Why would one start an article about fintech referencing Covid-19? The fact is that the virus is acting as both a headwind and tailwind for fintech companies operating from Ireland and internationally. The impact of the virus over the last month and a half on fintech has shone a spotlight on many aspects of the ecosystem that might not have otherwise come to our attention. In the current climate Ireland must also be mindful of any potential slippage of its position as a global fintech player garnered from recent years of excellent work. Let’s start with an overview of fintech. The word fintech came to prominence after the last financial crisis, particularly noticeable from 2012 onwards. Yet there were many examples of ‘financial technology’, shortened to “fintech”, existing well before the start of the last financial crisis. A number of these fintech businesses date back to the latter part of the 1980’s. Examples include the internet and phone retail bank First Direct[1] (a division of HSBC) which kicked off in 1989 and today regularly achieves high satisfaction rates in financial surveys. Ireland too served as HQ to a pioneer challenger bank, First-e[2] [6], which despite great promise was a casualty of the dot.com boom[3]. What does the Irish fintech scene look like? The consensus is that Ireland is home to somewhere between 220-250 indigenous fintech companies and that together with international fintech companies in Ireland, the number is probably around 400. It is difficult to give an exact figure if only because the word “fintech” is a broad-church. The word captures, (a) the new nonbank disruptors which focus on discrete parts of the banking value chain, e.g. payments, wealth management, treasury services and credit and lending; (b) the new breed of digital only (non-branch) challenger banks entering both retail and business banking; and (c) the incumbent banks (sometimes referred to as legacy banks) embarking - with various degrees of success – on digital transformation journeys. The recent release in April of the 2020 edition of the Fintech Ireland Map[4] identified 230 indigenous / Irish controlled fintech companies. This was an increase of 30% from the previous year. The Map is supported by both research and a survey[5]. The criteria to meet to join the Map is challenging. Entrants must be fintech companies with a proprietary product or service. Footnotes from above section - 1 https://en.wikipedia.org/wiki/First_Direct 2 https://en.wikipedia.org/wiki/First-e_Group 3 https://www.theguardian.com/money/2001/sep/08/saving.onlinebanking 4 https://fintechireland.com/fintech-ireland-map.html 5 https://fintechireland.com/fintech-survey.html  Broadly speaking the fintech companies operate across 12 categories, being Credit & Lending; Platforms; Funds & Trading; Crypto & Blockchain; FinOps (Financial Operations); InsurTech (Insurance Technology); Accounting; Payments; RegTech (Regulatory Technology); Savings / Investing; Big Data / Analytics; and Others. The number of firms in each category is shown in the diagram below. During 2019, the fintech ecosystem in Ireland, both the Republic of Ireland and Northern Ireland, continued to grow and evolve. There was strong growth in RegTech which not only increased to 39 companies but is rapidly closing in on Payments which retains its crown as the largest category for fintech companies, increasing to 58. It is no surprise that the Irish payments sector is so large given that it powers e-commerce transactions which by 2024 will double from 2010 to €3.8 billion in value. Also boding well for Ireland are two recent reports from UBS which estimate that global e-commerce will grow by 15-20% per annum over the next decade[7] from USD 3 trillion today. It is no wonder that global fintech revenue is expected to reach a staggering USD 500 billion by 2030[8]. The number of fintech firms in the Irish credit and lending sector grew in 2019, with the addition of six new entrants, to 23. This is positive news for cash strapped small-medium size enterprises. Hopefully these fintech companies will help fill the supply of liquidity which is currently in demand by cash-strapped businesses. Headwinds and Tailwinds The coronavirus crisis and its impact upon fintech is no different than the impact of the virus on other sectors of the economy. However, being a broadchurch, there are just as many fintech’s flourishing as there are floundering. FinTech’s, on average, didn’t begin 2020 with large amounts of equity. In fact, before Covid-19 the level of global investment in fintech dropped between 2018-2019 while the level of venture capital investment in Irish fintech fell off a cliff edge. In some cases, Irish fintech companies who had struck deals with international purchasers had to reduce the price to reflect, in the words of one fintech purchaser, the “economic reality” that businesses and individuals are currently facing. E-commerce companies and the fintech companies which process their payments have seen a significant fall in transaction volume and therefore revenue (processing fees) for travel related items, including airfares, hotels, holiday clothing, luggage and pre-paid travel vouchers. Whereas the fastest growing category of products and services includes – no surprises – disposable gloves, bread machines, cough & cold medicines as well as fitness equipment[9]. Thus, be wary about reading too much into e-commerce and payments processing growth, because it is not all good news. Having said that one of the most well-known e-commerce marketplaces specialising in crafted and homespun goods enjoyed a 100+% increase in share price in less than two months owing to demand for face masks! The World Bank predicts that global remittances from wealthy to poorer countries will drop by at least 20% to $445 billion. This represents a loss of a crucial financing lifeline for many vulnerable households. Much of this money is often eaten by fees by various middlemen. It is estimated that between 7% -12% of the money being transferred [10] is swallowed up by bank collection, transfer and receiving fees. Yet remittances are a vital source of income for people in developing countries. The loss of USD 10 from the value chain may mean the difference of food on the table for a family for a week in the poorest of countries. This challenge also provides an opportunity for fintech companies which can perform foreign exchange and international money transfers at a much lower cost than banks. Footnotes from above section - 6 https://en.wikipedia.org/wiki/First_Direct 7 https://www.ubs.com/global/en/wealth-management/chief-investment-office/investment-opportunities/longer-term-investments.html 8 https://fintechnews.ch/fintech/fintech-revenues-to-reach-us500b-by-2030-ubs-research/35500/ 9 https://www.visualcapitalist.com 10 This is a conservative estimate of fees. In some cases, the fees can be higher when cash is being handled at the collection and reception points  Another disruptor in this area is cryptocurrency. Cryptocurrency service providers remit crypto currency11, instead of fiat currency[12], and do so on distributed ledger technology – the most commonly known example being blockchain – which is simply a different set of payment rails than that used by the banks for money movement, such as SWIFT, the UK’s Faster Payments and Europe’s SEPA. Proponents of cryptocurrency for money transfers argue that it is 250 times cheaper on average to use cryptocurrency than traditional banks and is also cheaper than using many fintech apps.

There are less than ten indigenous crypto/blockchain fintech companies operating in Ireland. In recent years they have been joined by about half a dozen large international crypto/ blockchain firms focussed on financial services. Collectively these international companies are valued in the tens of billions of dollars. Like the indigenous companies, these international fintech’s have chosen Ireland to access our highly skilled software engineers, software developers, coders, programmers and data scientists. Noting the Irish government’s support of both blockchain and international financial services, we should expect to see a lot more from this nascent and promising industry in Ireland. Ireland is already perceived as a top global fintech ecosystem. Our challenge is not about reaching the number one spot globally, which simply will not be the case for a small open economy regardless of how progressive we are. Our challenge is to incrementally raise our profile and position year on year and more importantly remain in the upper echelons vis-à-vis our European Union peers. Ireland is home to 10,000+ regulated financial services companies, it is the 4th largest exporter of financial services in the European Union, 250 of the world’s largest financial services institutions have a base here including half of the world’s top 50 banks. With more than 45,000 people employed directly in international financial services, 15% of which work in fintech, is it any wonder that Dublin ranks 5th highest amongst the top 50 European cities according to Findexable Global Fintech Index 2020 and 7th highest ranked EU member state on the OECD’s Ease of Doing Business Index 2019. The future looks bright for Irish fintech. Many of these companies work in regulated markets and a number of these companies are authorised by the Central Bank of Ireland. What they have in common is the need for capital, people and a stable political environment. Ireland benefits from being a member of the European Union. It is an English first speaking language country, enjoys a common law legal system and adheres to the International Financial Reporting Standards. Ireland’s accountancy profession has a lot to offer and gain from Ireland’s fintech ecosystem. Whether it is a young fintech start-up requiring business and financial advice, seed funding, interim CFO services or larger fintech operator with important financial, taxation and HR strategic planning needs, a competent accounting professional is not only the corner stone but indeed the foundation of a successful and sustainable fintech. Footnotes from above section - 11 Examples of two cryptocurrencies include bitcoin and ethereum 12 Fiat currency is legal tender backed by a government, such as USD, EURO and GBP

Back to Blog

Bank of Lithuania's guidelines, opinion and position on security tokens, virtual assets and ICOs3/6/2020 Our blog of yesterday (02/06/2020) which was highlighted by Peter Oakes in his Linkedin account yesterday was been viewed 3,500+ times in less than a day*. Thanks for your interest in the topic of "Lithuanian Central Bank gives banks guidelines on opening accounts for electronic money and payment institutions."

By the way, for those interested in #tokens, #virtualassets and initial coin offerings (#ICOs), Lietuvos bankas / Bank of Lithuania has released a number of relevant documents in this space, worthy of a read, including:

If a problem with the above links, try to access via https://www.lb.lt/en/bank-of-lithuania-positions-and-guidelines See Linkedin Post at https://www.linkedin.com/posts/peteroakes_lithuania-electronicmoney-paymentinstitutions-activity-6673647923059798016-CBqg

Back to Blog

CompliReg's Peter Oakes joins Shilpa Arora, AML Director - Europe, Middle-East and Africa at ACAMS 24+ Financial Crime Marathon (2 & 3 June 2020) to discuss The Latest and Greatest in the World of Fintech.

Click here to watch the video

Back to Blog

The Bank of Lithuania (the Lithuanian central bank) (BoL) has issued its position paper on the right of electronic money institutions (EMIs) and payment institutions (PIs) to access bank accounts. You can download the position paper here.

Releasing the position paper, Jekaterina Govina, Director of the Supervision Service of the BoL said: “We hope that this position, agreed on with all market participants, will provide more clarity and help fintechs operate more smoothly as well as allow banks to improve their cooperation with such companies, while maintaining high risk management standards". Whilst the position paper is not an official interpretation of legislation, it is issued to support the right of institutions to access bank accounts opened with credit institutions and being necessary for their activities as stipulated in Article 10 of the Republic of Lithuania Law on Payments. Thus although the institutions have the right to apply to a credit institution for, for example, the opening of a payment account, there is no legal obligation on a credit institution to open said account for the institution. The position paper seeks to draw the attention of banks operating in Lithuania to the fact that some of their decisions regarding rejection to open accounts and/or unilaterally closing them, and/or applying restrictions on their access may cause negative consequences for EMIs/PIs and limit their licensed activities. The BoL notes that such decisions are often based on banks’ goal to properly manage the risk of money laundering and/or terrorist financing. The position paper doesn't seek to supplant banks' risk based decisions about which EMIs/PIs that they are prepared to give accounts to and to keep operating. This is rightly understandable especially noting that some banks may be concerned that the regulator has recently fined Lithuanian EMIs/PIs for various failures, including money laundering compliance. If you are a bank and you are processing payments for an EMI/PI, providing safeguarding for the EMI's/PI's clients and/or holding the EMI's/PI's ' corporate money and you have valid concerns about their compliance, you might ask yourself would it be wise to service this industry? Recent examples of fines against EMIs/PIs include:

Anyway, getting back to the position paper, it aims to ensure that while banks manage their own risks, banks do not violate the right of EMIs/PIs to have accounts with credit institutions and to access them. The specific type of accounts referenced in the position paper are:

A question we have, and we are sure many bank executives will be vexed by is: "How does a bank reconcile not only the desire of the BoL but at the same time protect its reputation, its shareholders and most importantly the financial system from financial crime?" An obvious starting point is to avoid the mindset that despite a particular financial sector being considered risker, it is OK to apply a carte blanche policy of refusing to provide players within that sector an account (or terminate their account). As the BoL puts it "banks must comply with the principles of objectivity, non-discrimination and proportionality in respect to EMIs/PIs, i.e. to ensure that their decisions and other actions relating to the opening (or closing) of accounts are impartial and objective". Or in other words (actually the words of the BoL) banks should ensure that:

are applied only after having assessed the circumstances relevant in a specific case and only when it is impossible to apply other risk management and mitigation measures. Yet we wonder, noting that the Lithuanian National Risk Assessment for Money Laundering and Terrorist Financing (released 28 May 2020) (LNRA) places payments/electronic money in the third highest category (of eight categories) for money laundering and terrorist financing threat and vulnerability, how quickly banks will not only adopt the BoL position paper but demonstrably work towards achieving the desired outcome? You can download the LNRA here. The position paper will no doubt be warmly welcomed by the 71 Electronic Money Institutions and 45 Payment Institutions which operate in Lithuania as at 25 May 2020. According to the Bank of Lithuania, the country ranks first in continental Europe in terms of licensed EMIs. This blog written by Peter Oakes. Peter advises on Lithuanian EMI/PI issues and advised on the authorisation of one Lithuania's first special bank authorisations. If you require a licence to operate in Lithuania, Ireland, Cyprus, Malta or the UK, see our Authorisation Page. We have a great network of experts in each country too, from lawyers, to accountants to technical experts. And get in contact if you have a question about this blog. |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]