|

Back to Blog

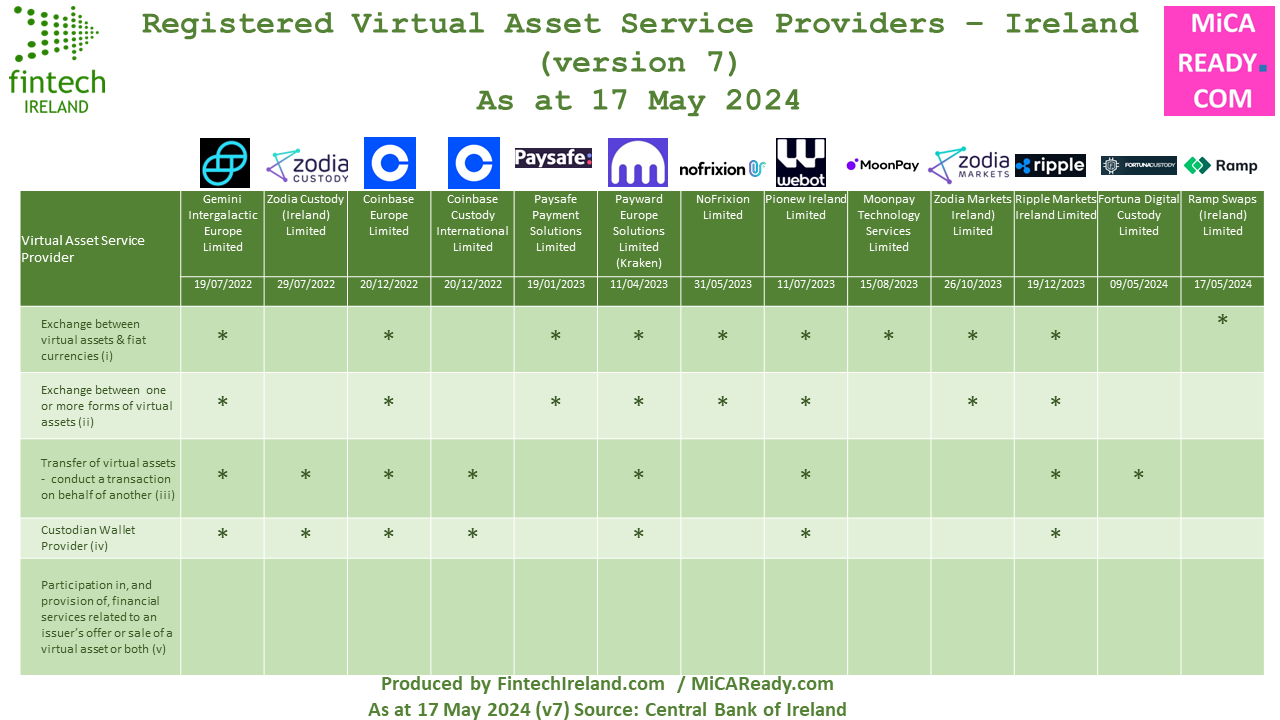

Central Bank of Ireland lays out its expectations of firms seeking crypto licensing in Ireland29/5/2024  If you are looking to get authorised under Markets in Crypto Asset Regulation (MiCAR) in Ireland, the Central Bank of Ireland has confirmed (or perhaps reconfirmed in some people's minds) that regulator intends to open its MiCAR authorisation gateway in early QUARTER 3 2024. While VASPs operating under the VASP regime prior to 30 December 2024, under MiCAR, will be permitted, post 30 December 2024, to avail of a transitional period enabling them to continue to operate for up to 12 months or until their CASP authorisation is granted or refused, whichever is sooner the CBI says that in respect of firms not yet registered as VASPs its experience is that period of at least ten months is required to conclude the assessment of a VASP application. The CBI says such firms should focus their efforts on preparing for a CASP application (under MiCAR) rather than seeking a VASP registration at this time. For those VASPs that have already applied for a registration but have not reached the end point of the process, the CBI will continue to assess these applications and will engage bilaterally with these firms on the progress of their applications. Following Ramp Swaps (Ireland) Limited's registration as a VASP, the latest such registration in Ireland, there are now 13 registered virtual asset service providers in Ireland and potentially a few more to come. Get in touch with CompliReg and see MiCA Ready if you are looking to get a MiCAR authorisation in Ireland or elsewhere in Europe.  Firms looking to get authorised in Ireland as a CASP or registered in near future as a VASP should note the following extracts from a speech today by Gerry Cross, Director for Financial Regulation, Policy and Risk at Blockchain Ireland's excellent event this week (see link at end of article)

Source: Technological innovation and financial regulation – a maturing relationship - Remarks by Gerry Cross, Director for Financial Regulation, Policy and Risk, Wednesday 29th May 2024 Linkedin Post: https://www.linkedin.com/posts/peteroakes_micar-virtualasset-activity-7201513163152834560-N6m7

0 Comments

Back to Blog

The announcement in the media that Coinbase is selecting Ireland as its EU regulatory headquarters has sparked quite a lot of discussion in crypto regulatory circles. Myself and a few others have been thinking about similarities between the race for a MiCAR authorisation [either from a standing start or from the position of already being a Virtual Asset Services Provider registrant in the EU] and the race for UK regulated firms needing an EU home post Brexit. In particular, I recall certain member states doing road shows on why a UK regulated firm should choose its country. While in Ireland, when challenged by the representative bodies and gatekeepers about doing more, the Central Bank of Ireland responded in speeches that it was in no one's interest to get involved in a race to the bottom. Will we not see something similar when it comes to MiCAR? Just because company A has a VASP registration in EU country A, it could make sense but, it doesn't necessarily follow that it will pursue a MiCAR authorisation in EU country A. That is more so the case, arguably, when they have VASP registrations in EU countries B, C and others (because there is no passporting). Therefore, and I am already seeing it myself, there are EU countries laying out their stall for your MiCAR authorisation regardless if you are (or not) already registered there as VASP. Some EU countries argue that their current VASP registration (& remember it was only ever intended to be a mere registration) is so robust and already aligned to MiCAR that you will find its offering a fast, efficient & effective way to getting the authorisation crown. I suspect other member states might take a political or supervisor risk-based decision not to exceed their obligations when dealing with a MiCAR authorisation and - potentially adding things into the authorisation process - to unintentionally but effectively killing-off an application. And, while it is great to hear of a large digital asset player laying down the marker that Ireland will be its EU regulatory home, I have lost count of how may MiFID, emoney and payment firms that have told me that "Ireland is the only country for our company", only to find that their view changes during the course of the authorisation process for whatever reason. I've seen companies apply elsewhere while pursuing an application in Ireland and I have spoken to some of those companies 18 months latter when they discovered the grass wasn't greener in the other EU member state. Against that backdrop, very interesting to read the Chair (Verna Ross) of European Securities and Markets Authority (ESMA) letter of 17 October 2023 to Nadia Calviño President of the Economic and Financial Affairs (ECOFIN) Council of the European Union, saying a number of important things about the MiCAR authorisation infrastructure. Of the many points made by ESMA in its letter, the following ones caught our eye.

The letter was cced to:

* Mairead McGuinness, Commissioner in charge of Financial Stability, Financial Services and Capital Markets Union, European Commission; * Irene Tinagli, Chair of the Committee on Economic and Monetary Affairs, European Parliament; * John Berrigan, Director-General, DG Financial Stability, Financial Services and Capital Markets Union, European Commission; * Thérèse Blanchet, Secretary-General of the Council of the European Union Union; * Claudia Lindemann, Head of the Secretariat of the Committee on Economic and Monetary Affairs, European Parliament

Back to Blog

Following the Permanent Representatives’ Committee meeting of 5 October 2022 which endorsed the final compromise text with a view to agreement, the Chair of the Committee (Edita Hrd) has written a letter and Proposal for a Regulation of the European Parliament and of the Council on Markets in Crypto-assets, and amending Directive (EU) 2019/1937 (MiCA) to the Chair of the Committee on Economic and Monetary Affairs (Irene TINAGLI) saying:

"that, should the European Parliament adopt its position at first reading, in accordance with Article 294 paragraph 3 of the Treaty, in the form set out in the compromise package contained in the Annex to this letter (subject to revision by the legal linguists of both institutions), the Council would, in accordance with Article 294. paragraph 4 of the Treaty, approve the European Parliament's position and the act shall be adopted in the wording which corresponds to the European Parliament's position." The full legal text of the landmark legislation known as the Markets in Crypto Assets Regulation (MiCA), alongside a further law to reveal the identity of those making crypto payments. At a Wednesday meeting (5th October 2022), diplomats representing the bloc's member governments in the EU's Council signed off on the text of laws (see link above) which were the subject of political deals struck in June. MiCA introduces the first-ever licensing regime for crypto wallets and exchanges to operate across the bloc and imposes reserve requirements on stablecoins that are intended to avoid Terra-style collapses. A separate law on funds transfers requires wallet providers to check their customer's identity, in a bid to cut money laundering. See also CoinDesk Article here |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]