|

Back to Blog

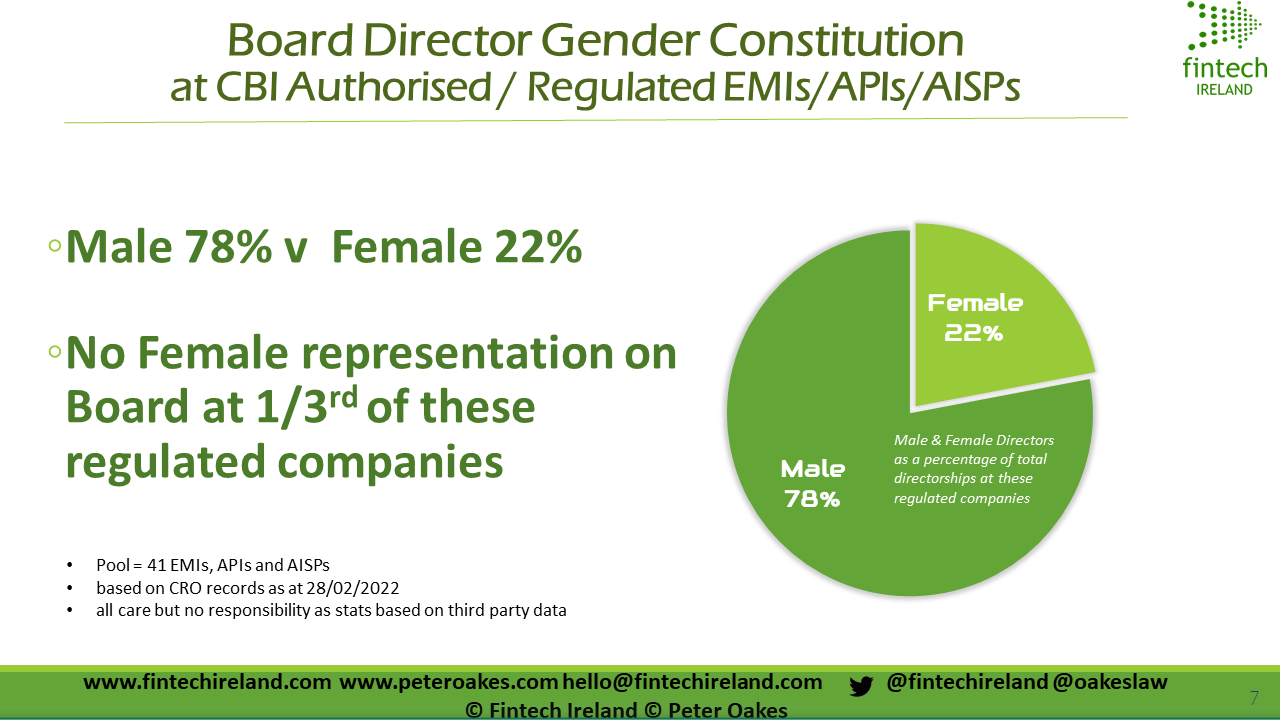

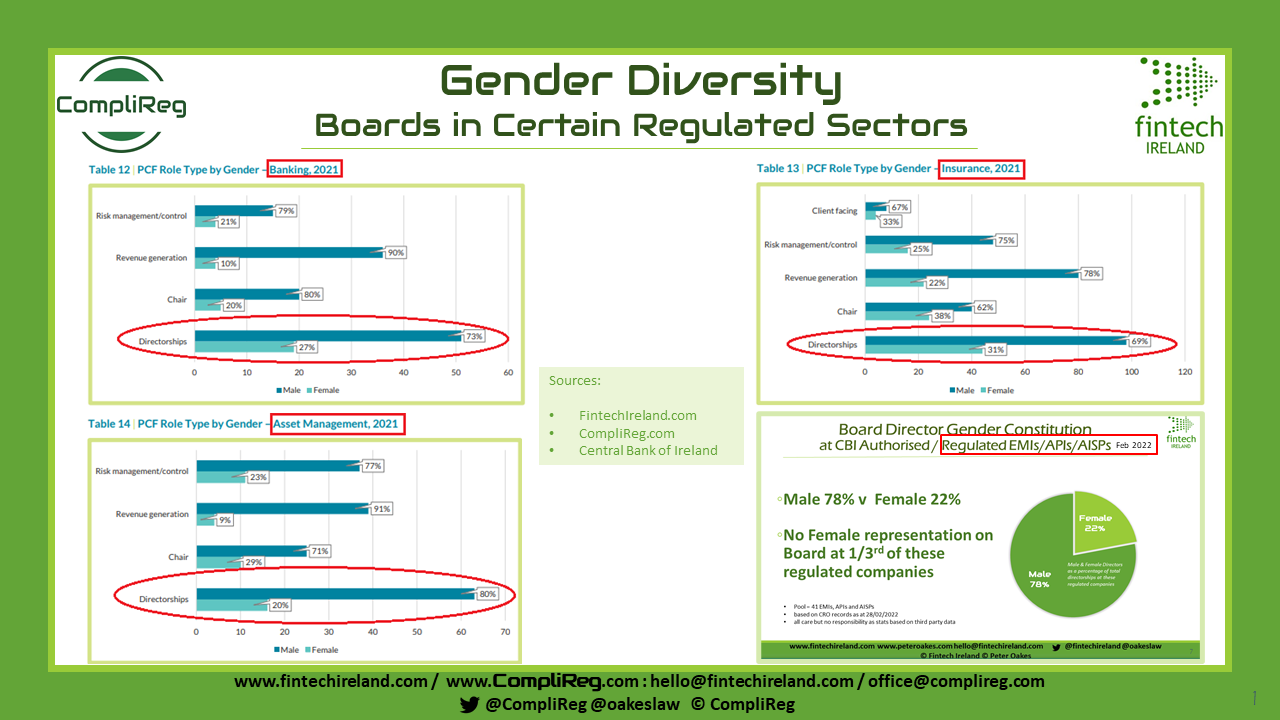

DOWNLOAD THE REPORT HERE “Regulated firms must prioritise diversity at senior levels to prevent groupthink, promote internal challenge, and protect consumers and investors” - Derville Rowland, Director General, Financial Conduct  Editor: According to the Central Bank of Ireland (see pages 21-23 of the Report), the male v female percentage split at Board director level in 2021 is: * Banking sector - 73% male v 27% female (table 12 of CBI report) * Insurance sector - 69% male v 31% female (table 13 of CBI report) * Asset Management sector - 80% male v 20% female (table 14 of CBI report) According to Fintech Ireland, the male v female percentage split at Board director level in February 2022 for authorised emoney and payments firms and registered account information service providers sector is 78% male v 22% female.  The above image is a curation of the Fintech Ireland and Central Bank of Ireland data. Gender diversity at senior levels in the regulated financial services sector is increasing but remains insufficient, according to the latest Central Bank of Ireland Demographic Analysis Report.

The annual publication analyses applications to hold certain senior roles within regulated firms that require the Central Bank’s prior approval under the Fitness & Probity Regime. The Central Bank received more than 3,500 such applications for Pre-Approval Control Function (PCF) roles in 2021. [NB: There are 53 Pre-Approval Controlled Functions, covering both board and management level appointments]. This is the sixth annual Demographic Analysis Report which breaks down the applications for regulatory approval by gender, age, and nationality. In addition to the 2021 analysis, today’s report also looks back at 10 years of PCF applications since the Fitness and Probity Regime took effect in 2012. Key developments outlined in the report include:

The analysis is primarily focused on gender diversity based on the data available. While this is only one form of diversity, it is a critically important one and also strongly indicative of wider diversity trends. Derville Rowland, Director General, Financial Conduct, said: “Whilst it is encouraging to see progress, it has been incremental over a decade, and firms simply must speed up. We remain of the view that a lack of diversity at senior management and board level is a leading indicator of heightened behaviour and culture risks. “Diversity extends beyond gender. Diversity, including age, ethnicity, educational and professional background, amongst other characteristics, is critical to developing an effective culture. Higher levels of diversity of thought can mitigate the risk of groupthink, improve decision-making, and increase the effectiveness of internal challenge and openness to change within firms. This is vital in terms of firms acting in the best interests of consumers and investors. “Given that diversity is so interconnected with risk, resilience and financial performance, it will continue to be a priority for the Central Bank.” Source: Central Bank of Ireland (08 March 2022)

0 Comments

Leave a Reply. |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]