|

Back to Blog

CompliReg's Peter Oakes joins Shilpa Arora, AML Director - Europe, Middle-East and Africa at ACAMS 24+ Financial Crime Marathon (2 & 3 June 2020) to discuss The Latest and Greatest in the World of Fintech.

Click here to watch the video

0 Comments

Back to Blog

The Bank of Lithuania (the Lithuanian central bank) (BoL) has issued its position paper on the right of electronic money institutions (EMIs) and payment institutions (PIs) to access bank accounts. You can download the position paper here.

Releasing the position paper, Jekaterina Govina, Director of the Supervision Service of the BoL said: “We hope that this position, agreed on with all market participants, will provide more clarity and help fintechs operate more smoothly as well as allow banks to improve their cooperation with such companies, while maintaining high risk management standards". Whilst the position paper is not an official interpretation of legislation, it is issued to support the right of institutions to access bank accounts opened with credit institutions and being necessary for their activities as stipulated in Article 10 of the Republic of Lithuania Law on Payments. Thus although the institutions have the right to apply to a credit institution for, for example, the opening of a payment account, there is no legal obligation on a credit institution to open said account for the institution. The position paper seeks to draw the attention of banks operating in Lithuania to the fact that some of their decisions regarding rejection to open accounts and/or unilaterally closing them, and/or applying restrictions on their access may cause negative consequences for EMIs/PIs and limit their licensed activities. The BoL notes that such decisions are often based on banks’ goal to properly manage the risk of money laundering and/or terrorist financing. The position paper doesn't seek to supplant banks' risk based decisions about which EMIs/PIs that they are prepared to give accounts to and to keep operating. This is rightly understandable especially noting that some banks may be concerned that the regulator has recently fined Lithuanian EMIs/PIs for various failures, including money laundering compliance. If you are a bank and you are processing payments for an EMI/PI, providing safeguarding for the EMI's/PI's clients and/or holding the EMI's/PI's ' corporate money and you have valid concerns about their compliance, you might ask yourself would it be wise to service this industry? Recent examples of fines against EMIs/PIs include:

Anyway, getting back to the position paper, it aims to ensure that while banks manage their own risks, banks do not violate the right of EMIs/PIs to have accounts with credit institutions and to access them. The specific type of accounts referenced in the position paper are:

A question we have, and we are sure many bank executives will be vexed by is: "How does a bank reconcile not only the desire of the BoL but at the same time protect its reputation, its shareholders and most importantly the financial system from financial crime?" An obvious starting point is to avoid the mindset that despite a particular financial sector being considered risker, it is OK to apply a carte blanche policy of refusing to provide players within that sector an account (or terminate their account). As the BoL puts it "banks must comply with the principles of objectivity, non-discrimination and proportionality in respect to EMIs/PIs, i.e. to ensure that their decisions and other actions relating to the opening (or closing) of accounts are impartial and objective". Or in other words (actually the words of the BoL) banks should ensure that:

are applied only after having assessed the circumstances relevant in a specific case and only when it is impossible to apply other risk management and mitigation measures. Yet we wonder, noting that the Lithuanian National Risk Assessment for Money Laundering and Terrorist Financing (released 28 May 2020) (LNRA) places payments/electronic money in the third highest category (of eight categories) for money laundering and terrorist financing threat and vulnerability, how quickly banks will not only adopt the BoL position paper but demonstrably work towards achieving the desired outcome? You can download the LNRA here. The position paper will no doubt be warmly welcomed by the 71 Electronic Money Institutions and 45 Payment Institutions which operate in Lithuania as at 25 May 2020. According to the Bank of Lithuania, the country ranks first in continental Europe in terms of licensed EMIs. This blog written by Peter Oakes. Peter advises on Lithuanian EMI/PI issues and advised on the authorisation of one Lithuania's first special bank authorisations. If you require a licence to operate in Lithuania, Ireland, Cyprus, Malta or the UK, see our Authorisation Page. We have a great network of experts in each country too, from lawyers, to accountants to technical experts. And get in contact if you have a question about this blog.

Back to Blog

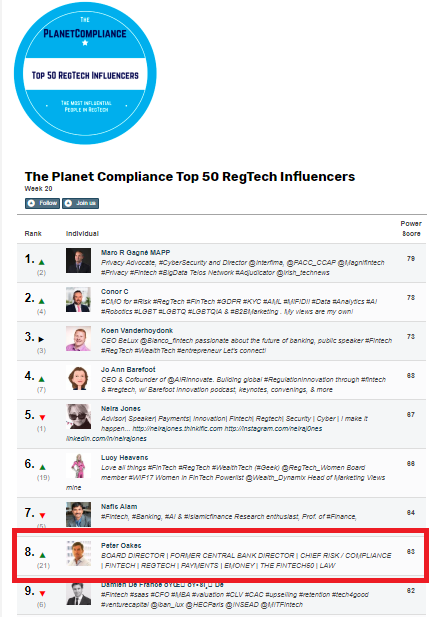

Yet again, our Peter Oakes, Non-Executive Director FinTech & FinServ and Founder of CompliReg and Fintech Ireland ranked in Top 10 of of the Top 50 RegTech Influencers. Planet Compliance updates a list of people that it finds are the key influencers in the field of RegTech. You'll find Peter Oakes featured almost every week in this list of RegTech influencers.

Peter was identified by the prestigious Chambers & Partners in January 2020 as leading band 1 FinTech advisor too.

Back to Blog

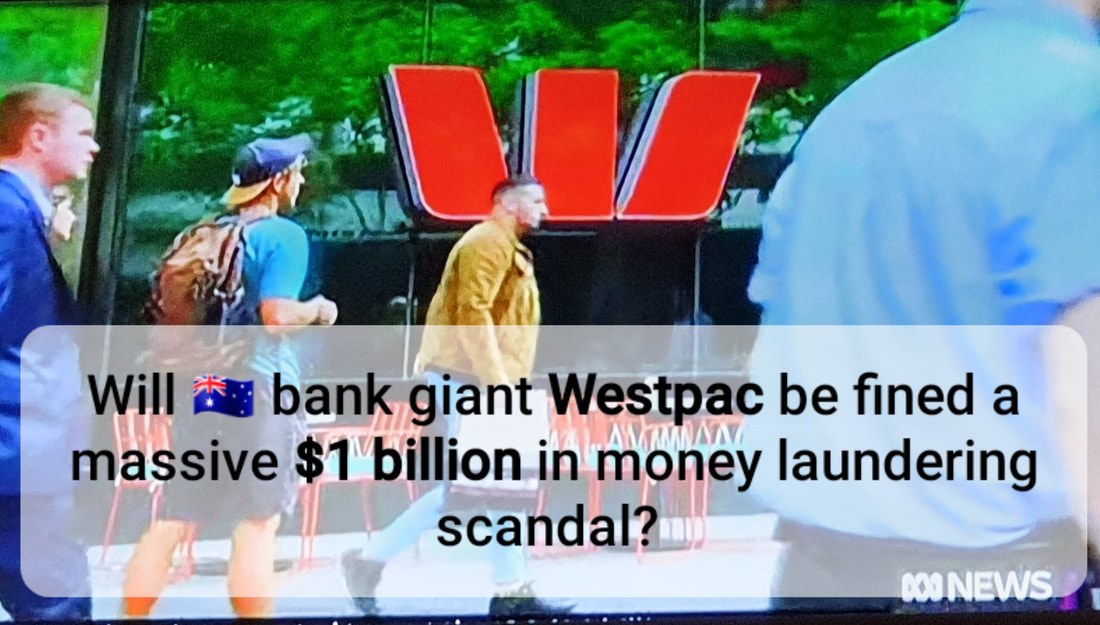

Australian Bank giant Westpac is expecting to fork out more than $1 billion as a result of its money laundering scandal and admitting to 23 million anti-money laundering breaches.

It's not just story about culture, conduct risk and financial crime risks. Far more importantly, it is a story of shame, leadership failure and financial pain for Westpac and relief for another Aussie bank. The fine would be the biggest corporate fine in Australian history. Westpac has revealed it expects the ongoing AUSTRAC investigation will cost it $1.03 billion. Such a fine will represent about 15% of the bank's 2019 profit. Shame: In November last year AUSTRAC, the entity responsible for preventing financial crimes, said the bank had violated anti-money laundering and counter-terrorism laws more than 23 million times (which the bank admits), allowing money tied to child exploitation in south-east Asia to flow freely. For example, Westpac's system was used by paedophiles to send money to the Philippines to pay for child abuse material without raising any red flags. Notwithstanding Westpac's admission, the bank is not going down without a fight. In the 57-page defence document filed with the court, Westpac denied AUSTRAC'S accusation that it failed to identify activity indicative of child exploitation risks. Leadership Failure: The scandal brought down Westpac's leadership, forcing the resignation of chief executive Brian Hartzer and the early retirement of chairman Lindsay Maxsted. Financial Pain: Last year Australian financial press reported that a penalty or settlement of $2 billion or $3 billion would see its CET1 ratio falling below 10.5% meaning the bank would be forced into another equity raising. And the trouble doesn't stop there for Westpac as the corporate regulator, ASIC, is probing into Westpac's previous $2.5 billion equity raise. Relief: Commonwealth Bank will be delighted to pass the mantle of the indignity of Australia's current money laundering record fine of $700 million to Westpac (Commonwealth Bank was fined for systemically failing to report around 54,000 suspicious transactions made through its "intelligent deposit machines"). If you want more on the story from the media, there are updates on an almost weekly basis - soon I guess daily basis. Just use this link to keep track of the story: "Westpac Austrac money laundering fine". And add case to your case studies and typologies in your AML / CTF training for everything from CDD, transaction monitoring, risk assessment, culture, condusct risk and (lack of) crisis management. Peter Oakes, Founder, CompliReg Peter Oakes is an experience anti-financial crime, fintech and board director professional. He served as Ireland's first Director of Enforcement and Financial Crime Supervision at the Central Bank of Ireland (2010-2013) in the aftermath of the financial crisis, leading the investigation and enforcement efforts into the Irish banking industry. Peter is a regular contributor to, and moderator and panel member at, ACAMS events.

Back to Blog

European Supervisors Instructed to Challenge Banks More Frequently. Peter Oakes discusses this topic with Gabriel Vedrenne, ACAMS MoneyLaundering.com

CLICK HERE

Back to Blog

16 January 2020: Peter Oakes, Founder of CompliReg (and Founder of Fintech Ireland, Fintech UK, Fintech NI and US Fintech / USTechFin) has been recognised as a Leading Band 1 Consultant in Chambers & Partners’ 2020 Professional Advisers guide for FinTech – the premier ranking of professional advisers to the financial services industry.

Peter secured a nationwide Ireland Band 1 ranking – Chambers’ top-tier ranking – where it was noted that: Peter Oakes, who has vast international regulatory experience as a former director of the Central Bank of Ireland. A source says: ‘Peter is high-profile, he has very strong governance capabilities and is very good for a regulated FinTech company.' Peter is a non-executive director of regulated fintech companies in the payments, e-money and MiFID sectors and is an adviser and mentor to fintech and regtech startups and scaleups. In Ireland he is a consultant to Clark Hill and in the UK he is a consultant to Kerman & Co, which is supporting the Fintech UK project. Learn more about Peter Oakes’s rankings in the Chambers FinTech guide here: https://chambers.com/department/peter-oakes-consulting-fintech-49:2743:114:1:23173986

Back to Blog

EU inches towards uniform AML rules and supervision. Peter Oakes discusses this topic with Gabriel Vedrenne, ACAMS MoneyLaundering.com

CLICK HERE

Back to Blog

If the United Kingdom's planned exit from the EU has complicated the lives of bankers, perhaps they can enjoy a little schadenfreude at the expense of the frequent bogeyman of their profession: bank regulators, who must now supervise the partial or wholesale relocation of scores of financial institutions from Great Britain to the bloc.

Peter Oakes discusses this topic with Gabriel Vedrenne, ACAMS MoneyLaundering.com CLICK HERE |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]