|

Back to Blog

I am sure there will be opposing views, but delighted for fintech and innovative finserv in both the UK and Ireland being thrown a commonsense method to continue the transfer of personal data between the UK and Ireland with the European Commission giving the green light to data transfers between EU countries and the UK. This happened yesterday via the European Commission adopting two adequacy decisions for the United Kingdom, one under the General Data Protection Regulation and the other under the Law Enforcement Directive. I posted on the previous draft versions a while ago on Linkedin. In summary, this means that personal data can now flow freely between Ireland and the UK, with the Commission guaranteeing citizens that their data in the UK has “essentially the equivalent level of protection to that guaranteed under EU law”. As seems with everything involving dealings between the UK and Europe, the resolution was found at minutes to midnight (so to speak) with the interim bridging mechanism which permitted personal data to be transferred from the EU to the UK following the end of the Brexit transition period, expiring on 30 June 2021. Essentially the Commission has assured citizens that GDPR will be fully respected in the UK. What does this mean for standard contractual clauses (SCCs)? The new adequacy decisions mean that personal data can continue to be transferred from the EU to the UK without additional steps such as the SCCs being put in place. “The UK has left the EU but today its legal regime of protecting personal data is as it was. Because of this, we are adopting these adequacy decisions today. At the same time, we have listened very carefully to the concerns expressed by the Parliament, the Members States and the European Data Protection Board, in particular on the possibility of future divergence from our standards in the UK's privacy framework. We are talking here about a fundamental right of EU citizens that we have a duty to protect. This is why we have significant safeguards and if anything changes on the UK side, we will intervene”. Věra Jourová, EC Vice-President for Values and Transparency, Key elements of the adequacy decisions

The adequacy decisions also facilitate the correct implementation of the EU-UK Trade and Cooperation Agreement, which foresees the exchange of personal information, for example for cooperation on judicial matters. Both adequacy decisions include strong safeguards in case of future divergence such as a ‘sunset clause', which limits the duration of adequacy to four years. “After months of careful assessments, today we can give EU citizens certainty that their personal data will be protected when it is transferred to the UK. This is an essential component of our new relationship with the UK. It is important for smooth trade and the effective fight against crime. The Commission will be closely monitoring how the UK system evolves in the future and we have reinforced our decisions to allow for this and for an intervention if needed. The EU has the highest standards when it comes to personal data protection and these must not be compromised when personal data is transferred abroad.” Didier Reynders, Commissioner for Justice Background

On 19 February, the Commission published two draft adequacy decisions and launched the procedure for their adoption. Over the past months, the Commission has carefully assessed the UK's law and practice on personal data protection, including the rules on access to data by public authorities in the UK. The Commission has been in close contact with the European Data Protection Board, which gave its opinion on 13 April, the European Parliament and the Member States. Following this in-depth process, the European Commission requested the green light on the adequacy decisions from Member States' representatives in the so-called comitology procedure. The adoption of the decisions today, following the agreement from Member States' representatives, is the last step in the procedure. The two adequacy decisions enter into force today (ie 28 June 2021). The EU-UK Trade and Cooperation Agreement (TCA) includes a commitment by the EU and UK to uphold high levels of data protection standards. The TCA also provides that any transfer of data to be carried out in the context of its implementation has to comply with the data protection requirements of the transferring party (for the EU, the requirements of the GDPR and the Law Enforcement Directive). The adoption of the two unilateral and autonomous adequacy decisions is an important element to ensure the proper application and functioning of the TCA. The TCA provides for a conditional interim regime under which data can flow freely from the EU to the UK. This interim period expires on 30 June 2021. Read more here

0 Comments

Back to Blog

How much does an #antimoneylaundering governance investigation cost a #fintech?

Previously noted that Australian EML doesn't expect a #moneylaundering compliance investigation (no allegation of money laundering) into one of its recently acquired Irish acquisitions (PFS Card Services Ireland Limited acquired in a deal worth up to €216.9m) to exceed AUD 2million / €1.27mn this Australian financial year which ends 30 June. However it cannot forecast the cost going into the next nor subsequent years. See https://lnkd.in/eg2cm82 (see previous blogs here). Well, it looks likely the costs may go higher if a class action by Shine Lawyers begins to bite, with the Aussie law firm looking for investors who bought shares between December 19, 2020, and May 17, 2021, to join its class action. The law firm says: * “EML did not request a trading halt for almost four days after learning of these concerns and then took another 48 hours to inform the market,” says Australian law firm * “When shareholders invest their money into a company, they do so with the belief that that company will comply with its continuous disclosure obligations. * “Our claim will allege that EML failed in its obligations, significantly impacting share prices for thousands of investors.” Read more by Sean Pollock at https://lnkd.in/efTj2dU Linkedin Post - https://www.linkedin.com/posts/peteroakes_antimoneylaundering-fintech-moneylaundering-activity-6809752916379922432-wNal

Back to Blog

Proposed 5 year strategy issued by Payment Systems Regulator.

The PSR's strategy sets out an approach that aims to make sure payments and payment systems work well for everybody and that there is fair competition and access to payments for all. The approach is to protect and embrace what’s working well, change what’s not, and lay the foundations for new products, ways to pay and new payment systems so that they develop with the needs of real people and businesses in mind. Key elements of the PSR Strategy The strategy sets out the PSR’s perspective on payment systems and the markets they support. It considers what is going well, where there is scope for improvement, and the risks and issues that need to be tackled.

What this looks like in practice In the strategy the PSR also sets out a number of actions it will take to deliver these priorities. Some of the key actions it is proposing include:

What happens next This document is a proposed strategy . The PSR is now seeking feedback from everyone with an interest in payment systems and how they work. The deadline for responding is 10 September 2021. This will help the PSR finalise its approach and ensure it is focused on the right outcomes, and - ultimately - have a strategy that is balanced and credible in the eyes of those its regulates and protects. As well as gathering written feedback the PSR is arranging a series of engagement events to listen and understand the views of its stakeholders. More information about these events can be found on its website. If you have any questions, please get in touch via [email protected] Links:

Back to Blog

EML Payments Money Laundering Governance Investigation to cost less than $2mn this financial year10/6/2021  In my previous post on EML Payments (EML) (see here) we noted that EML had advised that its Irish regulated subsidiary, PFS Card Services (Ireland) Limited ('PCSIL'), had received correspondence from the Central Bank of Ireland ('CBI'), including a letter received on Friday 14 May 2021 (Australian time) raising significant regulatory concerns ('Correspondence'). The CBI's concerns relate to PCSIL's Anti-Money Laundering / Counter Terrorism Financing ('AML/CTF'), risk and control frameworks and governance. The Correspondence states that the CBI is minded to issue directions to PCSIL pursuant to section 45 of the Central Bank (Supervision and Enforcement) Act 2013.

A few days ago, EML provided the Australian Stock Exchange with a trading update. The trading update also included its Quarter 3 FY2021 update in which EML confirmed: "Current Status:

Communication:

Business Impact:

Some observations:

Further reading - EML Payments Q3 FY21 Trading Update June 2021 (dated 7 June 2021)

Back to Blog

Received a letter from the Central Bank of Ireland's Anti-Money Laundering Division headed "AML Risk Evaluation Questionnaire (‘REQ’) Notification to [Name of Regulated Firm] (or ‘the firm’) to submit an REQ on an Annual Basis." last month with a return date this month? If so you are not alone.

The letter reminds that credit and financial institutions are required to have anti-money laundering (AML) and countering financing of terrorism (CFT) preventive measures to ensure compliance with the Criminal Justice (Money and Terrorist Financing) Acts 2010 to 2021, a well as reminding of the obligation to comply with EU Council Regulations setting out financial sanctions (‘FS’) measures. The CBI has established the REQ to seek information regarding individual firms’ exposure to Money Laundering / Terrorist Financing risks and also the AML/CFT compliance framework. Firms are being informed to submit the REQ in the specified format via the CBI's Online Reporting System on an ANNUAL BASIS within the time period specified on ONR. The CBI has informed firms that "for 2021, this deadline for the submission of the REQ return is 18 June 2021". Not only is the form detailed, and there are a few potential ways of interpreting some of the questions, or at least their interaction with other questions, but importantly for Boards of Directors note: i) Statement of Compliance: "... the REQ includes a statement to be signed by the firm confirming compliance with the firm’s AML/CFT/FS obligations. This statement if [sic] compliance should be signed and dated by a person who is duly authorised to do so by the Board (or equivalent). Ideally this person will have responsibility for AML/CFT/FS within the firm." NB this person doesn't need to be in a PCF role, but the CBI expect them to be of sufficient seniority within the firm to provide the confirmation sought. ii) Record Retention: "A record of the person who signed the statement of compliance must be formally noted in the Board minutes (or equivalent) when it is brought forward for consideration. The original signed and dated hard copy of the statement of compliance and the accompanying REQ is required to be kept on file and made available for review by the Central Bank on request." Need assistance with your risk assessment? Get in contact with us at the details here. Further reading: Risk Evaluation Questionnaire ('REQ') Return Building upon the obligations of credit and financial institutions under the CJA 2010, the Central Bank has developed a REQ in order to seek information regarding individual firms' exposure to ML / TF risks and also their AML / CFT compliance framework. Firms selected by the Central Bank to submit an REQ are required to submit the REQ in the specified format, through the Central Bank's Online Reporting System ('ONR'), within the time period specified on ONR. The minimum frequency that a firm will be required to submit an REQ is predicated on the level of ML/TF risk presented by the firm, either by virtue of its business model and/or the sector into which it falls (for further information on the frequency of submission please see the Table: AML/CFT Minimum Supervisory Engagement Model on the Central Bank AML / CFT Supervision Tab).

Linkedin Post: https://www.linkedin.com/posts/peteroakes_antimoney-aml-cft-activity-6808437129467756546-vRba

Back to Blog

Ireland's Finance Minister, Paschal Donohue, Speech on blockchain, crypto, fintech & innovation24/5/2021  A few short interesting extracts from a speech by Minister of Finance Paschal Donohoe to Blockchain Ireland audience yesterday (24 May 2021), covering fintech, payments, blockchain and crypto. Download the speech in PDF here

Full speech: Speech to Blockchain Ireland Week 2021 (Department of Finance)Published on 24 May 2021 Last updated on 24 May 2021 From Department of Finance Published on 24 May 2021 Last updated on 24 May 2021 Check Against Delivery Good morning everyone. I am delighted to be speaking to you today, albeit virtually, as part of Blockchain Ireland Week. First of all, I would like to acknowledge the commitment of Dave Feenan to blockchain; accepting the role as the new Chair of Blockchain Ireland, a challenge that few could have met. I would also like to acknowledge the tenacity and perseverance of Lory Kehoe, being one of the original founders of Blockchain Ireland, over 5 years ago. Thank you also Toomas Ilves for sharing your experience in the digitalisation of your country, and your expert understanding of blockchain technology. An inspiration for us all here, as this week we explore how we can create our present, and our future, working with this technology. It is hard to believe it is two years ago since I had the opportunity to meet many of you personally at the Iveagh Garden hotel. A lot has changed since, even the price of Bitcoin. Or should I say Dogecoin? Advances in the sector Blockchain Ireland Week is taking place at a crucial moment. The last year has been extremely difficult for everyone and the impact of Covid19 on our economy and society has been immense. Now, as our country begins to re-open and we continue to accelerate the vaccination programme, there is a sense of collective relief; we can allow ourselves to look forward more positively. Necessity is the mother of invention. You could say, necessity is the mother if innovation. And this is the moment to dare conceive new business models, engage with disruptive technologies and challenge ourselves to change and adapt. Because we need to change: as citizens, as customers, as businesses. We have all felt the need to adapt to the extreme circumstances of the pandemic. And we must continue to adjust; not to survive, but to thrive. The series of events that you, Blockchain Ireland, have scheduled for this week, offer an ample opportunity to learn more and explore how blockchain technology can improve our business, and our lives. Not only in Ireland, but within the EU, and globally. I wished I had the time to attend most of the events lined up for this week: the breadth and depth of topics being discussed is a testament to the leadership of Blockchain Ireland. International speakers from Africa, Asia, Australia, Europe and the United States will share their respective views and experiences. An extended thanks to all those speakers for bringing their expertise to our shores. From within Ireland, it’s fantastic to see how this technology is being used in initiatives such as: – Provenance in craft-beer, food and agricultural products – Making investing in bloodstock more affordable and transparent; – Providing integrity and trust to health data; – Exploring education and training choices. Right now, I would like to share with you two thoughts that struck me as I read about Blockchain Ireland week. The Benefits of Blockchain First, the discussion is no longer about “What is Blockchain?”, “Blockchain vs Crypto” or “Risks and benefits of Blockchain”. To me, this is a very encouraging sign. It demonstrates that the technology is maturing. We are increasingly seeing more instances of how the technology can benefit the economy and society; more enterprises are funding pilots; more private sector consortia are being created; we also see mainstream adoption starting to take off. The technology’s broad market applicability and the relevance to specific sectors is becoming clearer. It also demonstrates that in Ireland we are keeping abreast with changes in the technology. We have moved from 50 companies in Ireland working with blockchain back in May 2019 (when I last spoke to you), to almost 100 today: a sure sign that the Blockchain sector in Ireland is becoming more embedded in our ecosystem. My question for you all is: is that enough though? Could we do more? Could we do better? If so, what do we need to do? One of Ireland’s strengths is our ability to innovate and adapt to emerging trends across finance and technology and I have spoken before about the importance of nurturing Ireland’s knowledge economy. As a Government, we have tried to ensure that Ireland is prepared to take the advantages of technological opportunities though a number of interconnected initiatives. These objectives underpinned the Government’s Future Jobs Ireland strategy. Our vision, as set out in the Ireland for Finance Strategy to 2025, is for Ireland to remain internationally competitive and a top-tier location of choice for specialist IFS. We have a track record in this country for building globally recognised payment companies and innovative financial services businesses. As you will discuss this week, blockchain can transform the way in which many financial services sectors currently operate and deliver services to customers. The digital asset sector is becoming an increasingly competitive environment, while creating challenges for existing legal and supervisory frameworks, trying to match market and client requirements. We are actively monitoring developments in the technology and regulations globally, so that any potential policy changes will be crafted from a balanced, measured and carefully laid out review of risks and opportunities, both to consumers and to the economy. However, the pace of development is fast and the consequences of change might be difficult to comprehend early on. Thus, whether it is through the provision of digital assets or innovative ways of providing micro-insurance, I encourage you all to raise any concerns that would impede Ireland’s ability to remain competitive and a destination of choice for financial services. It is also encouraging to see how applications of the technology are being explored across the spectrum of our society. FutureNeuro, the Science Foundation Ireland Research Centre for Chronic and Rarer Neurological Diseases, is using blockchain to match sick patients to clinical trials based on their clinical and genomic data. It received €3.9 million in funding from the recent Disruptive Technology Innovation Fund award under Project Ireland 2040. Blockchain is also enabling innovative approaches to educational credentialing in the Irish banking sector. Earlier this year I was delighted to mark the launch of the EdQ Platform, a collaboration of the Institute of Banking alongside Bank of Ireland, AIB, Ulster Bank and Deloitte. This unique blockchain-based education credentialing platform for financial services is the first of its kind Ireland – and perhaps the world. Finally, there are 12 educational institutions across Ireland that are supporting and researching blockchain, whether that is in the form of ongoing research, study programmes or partnerships with other companies. Another heartening sign that Ireland is collectively working towards strengthening its knowledge economy credentials, anchoring on blockchain technology. To summarise, it is very inspiring to see evidence in the Irish blockchain sector that we are moving at pace with the maturity stages of the technology. As Minister for Finance, I would add that I am very reassured to see my Department has closely followed the pace and continues to be an integral participant of the Irish Blockchain Ecosystem. Trust in a Global Pandemic My second thought, is inspired by the central theme of this week’s event, “Blockchain: Foundation of Trust”. The pandemic has certainly accelerated the move to transacting and living in a digital world: what might have taken 10 years has been achieved in 10 months. We have all adapted to a large part of our lives being carried out online. However, necessity to do so may have trumped “trust”. Perhaps the most visible example of this was people being forced to drop the use of cash and become proficient in digital payments. The necessity to transact a payment online forced many to implicitly “trust” in the process, without considering who the company offering such services is or what consumer protection safeguards are in place if something goes wrong. And this was the case for everyone, irrespective of age or digital proficiency. As people became more comfortable with making financial transactions online, the 24/7 availability and convenient access made the purchasing of cryptocurrencies more accessible to the public than ever. As Minister for Finance, I’m conscious that investing in cryptocurrencies continues to involve risks and that there must be adequate regulation to protect consumers in this regard. Equally, I recognise that the blockchain technology that underpins these currencies is being a catalyst for innovation in the financial services sector, particularly payments and capital markets. Not only has the pandemic upended many of our constructs of a “normal” society, it has also challenged our trust in everything around us. Fake news should not be the new normal. Online scams should not be the new normal. Unverifiable scientific data should not be the new normal. As Finance Minister, and as President of the Eurogroup, I take the issue of trust in our banking and payment system very seriously. This is why we are closely monitoring developments into the review of a potential Digital Euro and follow the ECB’s ongoing research into Central Bank Digital Currencies. At the same time, my Department is working with the EU Commission and the Presidency to bring forth a general agreement on the draft proposal for regulation for a Market in Crypto Assets. Discussions are progressing at pace, particularly considering the technicality and complexity of the proposal. Why is this important? Because I believe that clarity of the legal and regulatory perimeter applicable to cryptoassets will bring trust for consumers and companies to deliver and use such products and services, which in turn will generate trust in our governing institutions. Conclusion As Minister for Finance, I welcome you all to Blockchain Ireland Week and I really look forward to exploring the key outcomes of this week’s discussions. I am sure it is going to be a terrific week of events. ENDS Source: https://www.gov.ie/en/speech/50cac-speech-to-blockchain-ireland-week-2021/

Back to Blog

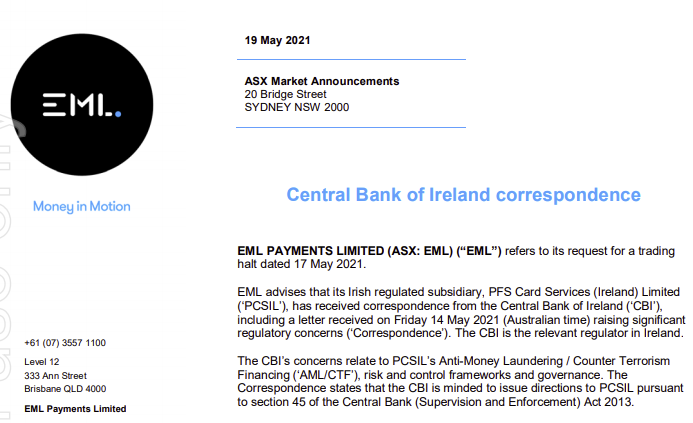

The ASX Market Announcement says:

"EML PAYMENTS LIMITED (ASX: EML) ("EMU') refers to its request for a trading halt dated 17 May 2021. EML advises that its Irish regulated subsidiary, PFS Card Services (Ireland) Limited ('PCSIL'), has received correspondence from the Central Bank of Ireland ('CBI'), including a letter received on Friday 14 May 2021 (Australian time) raising significant regulatory concerns ('Correspondence'). The CBI is the relevant regulator in Ireland. The CBI's concerns relate to PCSIL's Anti-Money Laundering / Counter Terrorism Financing ('AML/CTF'), risk and control frameworks and governance. The Correspondence states that the CBI is minded to issue directions to PCSIL pursuant to section 45 of the Central Bank (Supervision and Enforcement) Act 2013. The Correspondence does not concern EML's Australian or North American operations, or the operations of PFS' UK subsidiary ('Prepaid Financial Services Limited' which is incorporated in England and regulated by the FCA), or EML's other Irish regulated subsidiary ('EML Money DAC')." ASX Announcement in PDF and at source.

Back to Blog

The Financial Times reported that "EU policymakers round on Lithuania for lax fintech oversight" (18 May 2021).

In response Lithuania’s central bank insisted it was not “asleep at the wheel” over its regulation of a local fintech, that prosecutors suspect was used to steal more than €100m from Wirecard before it collapsed, and called for greater global sharing of information on financial crime among supervisors. On 19 May, the Financial Times wrote "Lithuanian central bank rebuffs Wirecard criticism" (19 May 2021). Read more at FintechLithuania.com

Back to Blog

UK FCA Dear CEO Letter - Emoney Firms ensure customers understand how their money is protected18/5/2021  On Tuesday 18th May 2021, the UK Financial Conduct Authority issued a Dear CEO Letter to Electronic Money Institutions headed "Please act: ensure your customers understand how their money is protected."

You can read a copy of the letter here. Some interesting excerpts from the letter below: What is the UK FCA concerned about?:

Action expected of emoney firms by the FCA:

Note the FCA point that the communication to customer be separate from any other messaging or promotional activity. And that the FCA expects emoney firms to consider the appropriate method(s) of communication based on their business model and customer base, including any vulnerable customers. Why should emoney action the letter?: Because the FCA intend to follow up, with a sample of firms, to assess the actions taken. Contact the team at CompliReg if you require assistance. You can read a copy of the letter here.

Back to Blog

“At the heart of our plans are more harmonised rules and a new AML Authority at EU level. The idea is to have common standards, common application and common supervision of our rules. That is as it should be in a single market.” European Union Commissioner Mairead McGuinness gave a speech yesterday (Monday 17th March 2021) at AMLintelligence.com Boardroom Series. Like other non-executive directors of regulated companies (obliged entities/designated persons), I took the time to read through the speech. Issues which caught my eye, not relevant just for traditional financial services, but indeed innovate one like fintech, are: A) Introduction:

B) AML Package: "At the heart of our plans are more harmonised rules and a new AML Authority at EU level. The idea is to have common standards, common application and common supervision of our rules. That is as it should be in a single market." Firstly,

Secondly,

If you are wondering about the impact this will have on the director supervisor of the financial sector, this is what Ms Guinness said:

How will the new Authority be funded?:

Why does the new AML Authority come to life?:

C: Other AML action:

"So these are busy times in the AML field. I genuinely believe that the work that we are doing now will lay solid foundations for a robust EU anti-money laundering and counter-terrorist financing regime which will stand the test of time. It is an absolutely vital task. Copy of Speech is located here.

Linkedin Post Here - https://www.linkedin.com/posts/peteroakes_virtualassets-finserv-regulation-activity-6800460598539816960-UBgz |

© CompliReg.com Dublin 2, Ireland ph +353 1 639 2971

| www.complireg.com | officeATcomplireg.com [replace AT with @]

| www.complireg.com | officeATcomplireg.com [replace AT with @]